lcd panel prices 2017 manufacturer

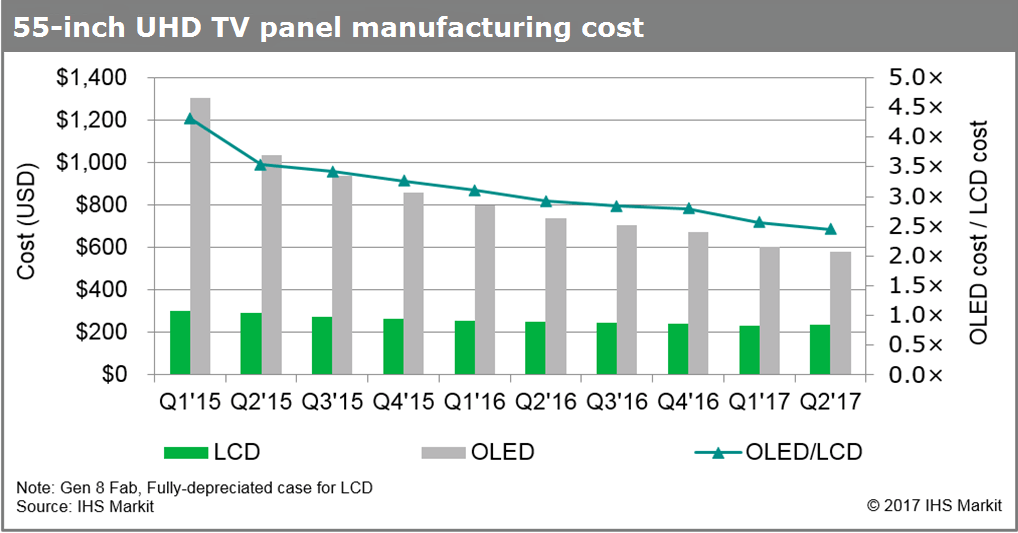

The statistic shows the manufacturing cost of a 55-inch ultra-high definition (UHD) TV panel from the first quarter of 2015 to the second quarter of 2017, broken down by technology. In the first quarter of 2017, the manufacturing cost of a 55-inch OLED UHD TV panel amounted to around 600 U.S. dollars per unit.Read moreManufacturing cost of a 55-inch UHD TV panel from 1st quarter 2015 to 2nd quarter 2017 (in U.S. dollars), by technologyCharacteristicLCDOLED---

Statista. (March 1, 2018). Manufacturing cost of a 55-inch UHD TV panel from 1st quarter 2015 to 2nd quarter 2017 (in U.S. dollars), by technology [Graph]. In Statista. Retrieved January 19, 2023, from https://www.statista.com/statistics/784279/55-inch-uhd-tv-panel-manufacturing-cost-by-technology/

Statista. "Manufacturing cost of a 55-inch UHD TV panel from 1st quarter 2015 to 2nd quarter 2017 (in U.S. dollars), by technology." Chart. March 1, 2018. Statista. Accessed January 19, 2023. https://www.statista.com/statistics/784279/55-inch-uhd-tv-panel-manufacturing-cost-by-technology/

Statista. (2018). Manufacturing cost of a 55-inch UHD TV panel from 1st quarter 2015 to 2nd quarter 2017 (in U.S. dollars), by technology. Statista. Statista Inc.. Accessed: January 19, 2023. https://www.statista.com/statistics/784279/55-inch-uhd-tv-panel-manufacturing-cost-by-technology/

Statista. "Manufacturing Cost of a 55-inch Uhd Tv Panel from 1st Quarter 2015 to 2nd Quarter 2017 (in U.S. Dollars), by Technology." Statista, Statista Inc., 1 Mar 2018, https://www.statista.com/statistics/784279/55-inch-uhd-tv-panel-manufacturing-cost-by-technology/

Statista, Manufacturing cost of a 55-inch UHD TV panel from 1st quarter 2015 to 2nd quarter 2017 (in U.S. dollars), by technology Statista, https://www.statista.com/statistics/784279/55-inch-uhd-tv-panel-manufacturing-cost-by-technology/ (last visited January 19, 2023)

Manufacturing cost of a 55-inch UHD TV panel from 1st quarter 2015 to 2nd quarter 2017 (in U.S. dollars), by technology [Graph], Statista, March 1, 2018. [Online]. Available: https://www.statista.com/statistics/784279/55-inch-uhd-tv-panel-manufacturing-cost-by-technology/

Prices for all TV panel sizes fluctuated and are forecast to fluctuate between 2020 and 2022. The period from March 2020 to July 2021 saw the biggest price increases, when a 65" UHD panel cost between 171 and 288 U.S. dollars. In the fourth quarter of 2021, such prices fell and are expected to drop to an even lower amount by March 2022.Read moreLCD TV panel prices worldwide from January 2020 to March 2022, by size(in U.S. dollars)Characteristic32" HD43" FHD49"/50" UHD55" UHD65" UHD------

DSCC. (January 10, 2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph]. In Statista. Retrieved January 19, 2023, from https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars)." Chart. January 10, 2022. Statista. Accessed January 19, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. (2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars). Statista. Statista Inc.. Accessed: January 19, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "Lcd Tv Panel Prices Worldwide from January 2020 to March 2022, by Size (in U.S. Dollars)." Statista, Statista Inc., 10 Jan 2022, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC, LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) Statista, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/ (last visited January 19, 2023)

LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph], DSCC, January 10, 2022. [Online]. Available: https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

LCD panel prices have risen for 4 months in a row because of your home gaming? Since this year, the whole LCD panel market has smoked. Whether after the outbreak of the epidemic, LCD panel market prices rose for four months, or the panel giants in Japan and South Korea successively sold production lines, or the Chinese mainland listed companies frequently integrated acquisition, investment, and plant construction, all make the industry full of interesting.

LCD panel prices are already a fact. Since May this year, LCD panel prices have risen for four months in a row, making the whole industry chain dynamic. Why are LCD panels going up in price in a volatile 2020? The key factor lies in the imbalance between supply and demand.

For larger sizes, overseas stocks remained strong, with prices for 65 inches and 75 inches rising $10 on average to $200 and $305 respectively in September.

The price of LCDS for large-size TVs of 70 inches or more hasn’t budged much. In addition, LTPS screens and AMOLED screens used in high-end phones have seen little or no increase in price.

As for October, LCD panel price increases are expected to moderate. The data shows that in October 32 inches or 2 dollars; Gains of 39.5 to 43 inches will shrink to $3;55 inches will fall back below $10; The 65-inch gain will narrow to $5.

During the epidemic, people stayed at home and had no way to go out for entertainment. They relied on TV sets, PCS, and game consoles for entertainment. After the resumption of economic work and production, the market of traditional home appliances picked up rapidly, and LCD production capacity was quickly digested.

However, due to the shutdown of most factories lasting 1-2 months during the epidemic period, LCD panel production capacity was limited, leading to insufficient production capacity in the face of the market outbreak, which eventually led to the market shortage and price increase for 4 consecutive months.

In fact, the last round of price rise of LCD panels was from 2016 to 2017, and its overall market price has continued to fall since 2018. Even in 2019, individual types have fallen below the material cost, and the whole industry has experienced a general operating loss. As a result, LCD makers have been looking for ways to improve margins since last year.

A return to a reasonable price range is the most talked about topic among panel makers in 2019, according to one practitioner. Some manufacturers for the serious loss of the product made the decision to reduce production or even stop production; Some manufacturers planned to raise the price, but due to the epidemic in 2020, the downstream demand was temporarily suppressed and the price increase was postponed. After the outbreak was contained in April, LCD prices began to rise in mid-to-late May.

In fact, the market price of LCD panels continued to decline in 2018-2019 because of the accelerated rise of China’s LCD industry and the influx of a large number of local manufacturers, which doubled the global LCD panel production capacity within a few years, but there was no suitable application market to absorb it. The result of excess capacity is oversupply, ultimately making LCD panel prices remain depressed.

Against this background, combined with the impact of the epidemic in 2020, the operating burden of LCD companies in Japan and South Korea has been further aggravated, and it is difficult to make profits in the production of LCD panels, so they have to announce the withdrawal of LCD business.

business in June 2022. In August, Sharp bought JDI Baishan, a plant in Ishikawa prefecture that makes liquid crystal display panels for smartphones. In early September, Samsung Display sold a majority stake in its SUZHOU LCD production plant to Starlight Electronics Technology, a unit of TCL Technology Group. LGD has not only pulled out of some of its production capacity but has announced that it will close its local production line in 2020. According to DSCC, a consultancy, the share of LCD production capacity in South Korea alone will fall from 19% to 7% between 2020 and 2021.

It is worth mentioning that in industry analysis, in view of the fact that Korean companies are good at using “dig through old bonus – selling high price – the development of new technology” the cycle of development mode, another 2020 out of the LCD production capacity, the main reason may be: taking the advantage of China’s expanding aggressively LCD manufacturers, Korean companies will own LCD panel production line hot sell, eliminating capacity liquid to extract its final value, and turning to the more profitable advantage of a new generation of display technologies, such as thinner, color display better OLED, etc. Samsung, for example, has captured more than 80% of the OLED market with its first-mover advantage.

From the perspective of production capacity, the launch of LCD tracks by major manufacturers in Japan and South Korea must reduce some production capacity in the short term, which to some extent induces market price fluctuations. In the long run, some of the Japanese and Korean LCD production capacity has been bought by Chinese manufacturers, coupled with frequent investment in recent years, the overall capacity is sure to recover as before, or even more than before. But now it will take time to expand the production layout, which more or less will cause supply imbalance, the industry needs to be cautious.

The LCD panel industry started in the United States and then gradually moved to Japan, South Korea, China, and Taiwan. At present, the proportion of production capacity in The Chinese mainland has reached 52% in 2020, and there are leading LCD panel products in China represented by BOE, Huxing Optoelectronics. Meanwhile, the production capacity layout of BOE, Huike, Huxing Optoelectronics, and other manufacturers has been basically completed, making industrial integration a necessity.

On the one hand, South Korean enterprises out of the LCD track, the domestic factory horse enclosure, plant expansion action. While LCDs may not sell as well as “upstart” flexible screens, respondents believe they are still strong enough in the traditional home appliance market to warrant continued investment. Zhao Bin, general manager of TCL Huaxing Development Center, has said publicly that the next-generation display technology will be mature in four to five years, but the commercialization of products may not take place until a decade later. “LCD will still be the mainstream in this decade,” he said.

On the other hand, there is no risk of neck jam in China’s LCD panel industry, which is generally controllable. In mainland China, there will be 21 production lines capable of producing 32-inch or larger LCD panels by 2021, accounting for about two-thirds of the global total. In terms of the proportion of production capacity, the Chinese mainland accounted for 42% of the global LCD panel in 2019, 51% this year, and will continue to climb to 63% next year.

Of course, building factories and expanding production cannot be accomplished overnight. In the process of production capacity recovery, it is predicted that there will be several price fluctuations, and the cost may be passed on to the downstream LCD panel manufacturers or consumers when the price rises greatly, which requires continuous attention.

Large LCD panel prices have been continuously increasing for last 10 months due to an increase in demand and tight supply. This has helped the LCD industry to recover from drastic panel price reductions, revenue and profit loss in 2019. It has also contributed to the growth of Quantum Dot and MiniLED LCD TV.

Strong LCD TV panel demand is expected to continue in 2021, but component shortages, supply constraints and very high panel price increase can still create uncertainties.

LCD TV panel capacity increased substantially in 2019 due to the expansion in the number of Gen 10.5 fabs. After growth in 2018, LCD TV demand weakened in 2019 caused by slower economic growth, trade war and tariff rate increases. Capacity expansion and higher production combined with weaker demand resulted in considerable oversupply of LCD TV panels in 2019 leading to drastic panel price reductions. Some panel prices went below cash cost, forcing suppliers to cut production and delay expansion plans to reduce losses.

Panel over-supply also brought down panel prices to way lower level than what was possible through cost improvement. Massive 10.5 Gen capacity that can produce 8-up 65" and 6-up 75" panels from a single mother glass substrate helped to reduce larger size LCD TV panel costs. Also extremely low panel price in 2019 helped TV brands to offer larger size LCD TV (>60-inch size) with better specs and technology (Quantum Dot & MiniLED) at more competitive prices, driving higher shipments and adoption rates in 2019 and 2020.

While WOLED TV had higher shipment share in 2018, Quantum Dot and MiniLED based LCD TV gained higher unit shares both in 2019 and 2020 according to Omdia published data. This trend is expected to continue in 2021 and in the next few years with more proliferation of Quantum Dot and MiniLED TVs.

Panel suppliers’ financial results suffered in 2019 as they lost money. Suppliers from China, Korea and Taiwan all lowered their utilization rates in the second half of 2019 to reduce over-supply. Very low prices combined with lower utilization rates made the revenue and profitability situation for panel suppliers difficult in 2019. BOE and China Star cut the utilization rates of their Gen 10.5 fabs. Sharp delayed the start of production at its 10.5 Gen fab in China. LGD and Samsung display decided to shift away from LCD more towards OLED and QDOLED respectively. Both companies cut utilization rates in their 7, 7.5 and 8.5 Gen fabs. Taiwanese suppliers also cut their 8.5 Gen fab utilization rates.

An increase in demand for larger size TVs in the second half of 2020 combined with component shortages has pushed the market to supply constraint and caused continuous panel price increases from June 2020 to March 2021. Market demand for tablets, notebooks, monitors and TVs increased in 2020 especially in the second half of the year due to the impact of "stay at home" regulations, when work from home, education from home and more focus on home entertainment pushed the demand to higher level.

With stay at home continuing in the firts half of 2021 and expected UEFA Europe football tournaments and the Olympic in Japan (July 23), TV brands are expecting stronger demand in 2021. The panel price increase resulting in higher costs for TV brands. It has also made it difficult for lower priced brands (Tier2/3) to acquire enough panels to offer lower priced TVs. Further, panel suppliers are giving priority to top brands with larger orders during supply constraint. In recent quarters, the top five TV brands including Samsung, LG, and TCL have been gaining higher market share.

From June 2020 to January 2021, the 32" TV panel price has increased more than 100%, whereas 55" TV panel prices have increased more than 75% and the 65" TV panel price has increased more than 38% on average according to DSCC data. Panel prices continued to increase through Q1 and the trend is expected to continue in Q2 2021 due to component shortages.

In last few months top glass suppliers Corning, NEG and AGC have all experienced production problems. A tank failure at Corning, a power outage at NEG and an accident at an AGC glass plant all resulted in glass supply constraints when demand and production has been increasing. In March this year Corning announced its plan to increase glass prices in Q2 2021. Corning has also increased supply by starting glass tank in Korea to supply China’s 10.5 Gen fabs that are ramping up. Most of the growth in capacity is coming from Gen 8.6 and Gen 10.5 fabs in China.

Major increases in panel prices from June 2020, have increased costs and reduced profits for TV brand manufacturers. TV brands are starting to increase TV set prices slowly in certain segments. Notebook brands are also planning to raise prices for new products to reflect increasing costs. Monitor prices are starting to increase in some segments. Despite this, buyers are still unable to fullfill orders due to supply issues.

TV panel prices increased in Q4 2020 and are also expected to increase in the first half of 2021. This can create challenges for brand manufacturers as it reduces their ability to offer more attractive prices in coming months to drive demand. Still, set-price increases up to March have been very mild and only in certain segments. Some brands are still offering price incentives to consumers in spite of the cost increases. For example, in the US market retailers cut prices of big screen LCD and OLED TV to entice basketball fans in March.

Higher LCD price and tight supply helped LCD suppliers to improve their financial performance in the second half of 2020. This caused a number of LCD suppliers especially in China to decide to expand production and increase their investment in 2021.

New opportunities for MiniLED based products that reduce the performance gap with OLED, enabling higher specs and higher prices are also driving higher investment in LCD production. Suppliers from China already have achieved a majority share of TFT-LCD capacity.

BOE has acquired Gen 8.5/8.6 fabs from CEC Panda. ChinaStar has acquired a Gen 8.5 fab in Suzhou from Samsung Display. Recent panel price increases have also resulted in Samsung and LGD delaying their plans to shut down LCD production. These developments can all help to improve supply in the second half of 2021. Fab utilization rates in Taiwan and China stayed high in the second half of 2020 and are expected to stay high in the first half of 2021.

Price increases for TV sets are still not widespread yet and increases do not reflect the full cost increase. However, if set prices continue to increase to even higher levels, there is the potential for an impact on demand.

QLED and MiniLED gained share in the premium TV market in 2019, impacting OLED shares and aided by low panel prices. With the LCD panel price increases in 2020 the cost gap between OLED TV and LCD has gone down in recent quarters.

OLED TV also gained higher market share in the premium TV market especially sets from LG and Sony in the last quarter of 2020, according to industry data. LG Display is implimenting major capacity expansion of its OLED TV panels with its Gen 8.5 fab in China.Strong sales in Q4 2020 and new product sizes such as 48-inch and 88-inch have helped LG Display’s OLED TV fabs to have higher utilization rates.

Samsung is also planning to start production of QDOLED in 2021. Higher production and cost reductions for OLED TV may help OLED to gain shares in the premium TV market if the price gap continues to reduce with LCD.

Lower tier brands are not able to offer aggressive prices due to the supply constraint and panel price increases. If these conditions continue for too long, TV demand could be impacted.

Strong LCD TV demand especially for Quantum Dot and MiniLED TV is expected to continue in 2021. The economic recovery and sports events (UEFA Europe footbal and the Olympics in Japan) are expected to drive demand for TV, but component shortages, supply constraints and too big a price increase could create uncertainties. Panel suppliers have to navigate a delicate balance of capacity management and panel prices to capture the opportunity for higher TV demand. (SD)

(2 November, 2017) – A major decrease in manufacturing cost gap between organic light-emitting diode (OLED) display and liquid crystal display (LCD) panel is expected to support the expansion of OLED TVs, according to new analysis from

analysis estimates that the total manufacturing cost of a 55-inch OLED ultra-high definition (UHD) TV panel -- at the larger end for OLED TVs -- stood at $582 per unit in the second quarter of 2017, a 55 percent drop from when it was first introduced in the first quarter of 2015. The cost is expected to decline further to $242 by the first quarter of 2021, IHS Markit said.

The manufacturing cost of a 55-inch OLED UHD TV panel has narrowed to 2.5 times that of an LCD TV panel with the same specifications, compared to 4.3 times back in the first quarter of 2015.

“Historically, a new technology takes off when the cost gap between a dominant technology and a new technology gets narrower,” said Jimmy Kim, principal analyst for display materials at IHS Markit. “The narrower gap in the manufacturing cost between the OLED and LCD panel will help the expansion of OLED TVs.”

However, it is not just the material that determines the cost gap. In fact, when the 55-inch UHD OLED TV panel costs were 2.5 times more than LCD TV panel, the gap in the material costs was just 1.7 times. Factors other than direct material costs, such as production yield, utilization rate, depreciation expenses and substrate size, do actually matter, IHS Markit said.

The total manufacturing cost difference will be reduced to 1.8 times from the current 2.5 times, when the yield is increased to a level similar to that of LCD panels. “However, due to the depreciation cost of OLED, there are limitations in cost reduction from just improving yield,” Kim said. “When the depreciation is completed, a 31 percent reduction in cost can be expected from now.”

by IHS Markit provides more detailed cost analysis of OLED panels, including details of boards, arrays, luminescent materials, encapsulants and direct materials such as driver ICs. The report also covers overheads such as occupancy rate, selling, general and depreciation costs. In addition, this report analyzes OLED panels in a wide range of sizes and applications.

IHS Markit is a registered trademark of IHS Markit Ltd and/or its affiliates. All other company and product names may be trademarks of their respective owners © 2017 IHS Markit Ltd. All rights reserved.

LCD TV Panel Market is 2022 Research Report on Global professional and comprehensive report on the LCD TV Panel Market. The report monitors the key trends and market drivers in the current scenario and offers on the ground insights. Top Key Players are – Samsung Display, LG Display, Innolux Crop., AUO, CSOT, BOE, Sharp, Panasonic, CEC-Panda.

Global “LCD TV Panel Market” (2022-2028) the report additionally centers around worldwide significant makers of the LCD TV Panel market with important data, such as, company profiles, segmentation information, challenges and limitations, driving factors, value, cost, income and contact data. Upstream primitive materials and hardware, coupled with downstream request examination is likewise completed. The Global LCD TV Panel market improvement patterns and marketing channels are breaking down. In conclusion, the attainability of new speculation ventures is surveyed and in general, the research ends advertised.

Global LCD TV Panel Market Report 2022 is spread across 117 pages and provides exclusive vital statistics, data, information, trends and competitive landscape details in this niche sector.

LCD displays utilize two sheets of polarizing material with a liquid crystal solution between them. An electric current passed through the liquid causes the crystals to align so that light cannot pass through them. Each crystal, therefore, is like a shutter, either allowing light to pass through or blocking the light. LCD panel is the key components of LCD display. And the price trends of LCD panel directly affect the price of liquid crystal displays. LCD panel consists of several components: Glass substrate, drive electronics, polarizers, color filters etc. Only LCD panel applied for TV will be counted in this report.

Due to the COVID-19 pandemic, the global LCD TV Panel market size is estimated to be worth USD 53490 million in 2021 and is forecast to a readjusted size of USD 53490 million by 2028 with a CAGR of 2.2% during the review period. Fully considering the economic change by this health crisis, by Size accounting for (%) of the LCD TV Panel global market in 2021, is projected to value USD million by 2028, growing at a revised (%) CAGR in the post-COVID-19 period. While by Size segment is altered to an (%) CAGR throughout this forecast period.

Global LCD TV Panel key players include Samsung Display, LG Display, Innolux Crop, AUO, CSOT, etc. Global top five manufacturers hold a share over 80%.

The global LCD TV Panel market is segmented by company, region (country), by Size and by Application. Players, stakeholders, and other participants in the global LCD TV Panel market will be able to gain the upper hand as they use the report as a powerful resource. The segmental analysis focuses on sales, revenue and forecast by region (country), by Size and by Application for the period 2017-2028.

Global LCD TV Panel market analysis and market size information is provided by regions (countries). Segment by Application, the LCD TV Panel market is segmented into United States, Europe, China, Japan, Southeast Asia, India and Rest of World. The report includes region-wise LCD TV Panel market forecast period from history 2017-2028. It also includes market size and forecast by players, by Type, and by Application segment in terms of sales and revenue for the period 2017-2028.

The report introduced the LCD TV Panel basics: definitions, classifications, applications and market overview; product specifications; manufacturing processes; cost structures, raw materials and so on. Then it analyzed the world’s main region market conditions, including the product price, profit, capacity, production, supply, demand and market growth rate and forecast etc. In the end, the report introduced new project SWOT analysis, investment feasibility analysis, and investment return analysis.

LCD TV Panel market size competitive landscape provides details and data information by players. The report offers comprehensive analysis and accurate statistics on revenue by the player for the period 2017-2021. It also offers detailed analysis supported by reliable statistics on revenue (global and regional level) by players for the period 2017-2021. Details included are company description, major business, company total revenue and the sales, revenue generated in LCD TV Panel business, the date to enter into the LCD TV Panel market, LCD TV Panel product introduction, recent developments, etc.

The report offers detailed coverage of LCD TV Panel industry and main market trends with impact of coronavirus. The market research includes historical and forecast market data, demand, application details, price trends, and company shares of the leading LCD TV Panel by geography. The report splits the market size, by volume and value, on the basis of application type and geography. Report covers the present status and the future prospects of the global LCD TV Panel market for 2017-2028.

Global LCD TV Panel Market report forecast to 2028 is a professional and comprehensive research report on the world’s major regional market conditions, focusing on the main regions (North America, Europe and Asia-Pacific) and the main countries (United States, Germany, United Kingdom, Japan, South Korea and China).

To Know How COVID-19 Pandemic Will Impact LCD TV Panel Market/Industry- Request a sample copy of the report-https://www.researchreportsworld.com/enquiry/request-covid19/21019731

The report offers exhaustive assessment of different region-wise and country-wise LCD TV Panel market such as U.S., Canada, Germany, France, U.K., Italy, Russia, China, Japan, South Korea, India, Australia, Taiwan, Indonesia, Thailand, Malaysia, Philippines, Vietnam, Mexico, Brazil, Turkey, Saudi Arabia, U.A.E, etc. Key regions covered in the report are North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

For the period 2017-2028, the report provides country-wise revenue and volume sales analysis and region-wise revenue and volume analysis of the global LCD TV Panel market. For the period 2017-2021, it provides sales (consumption) analysis and forecast of different regional markets by Application as well as by Type in terms of volume.

What are the market opportunities and threats faced by the vendors in the global LCD TV Panel market? What industrial trends, drivers, and challenges are manipulating its growth?

With tables and figures helping analyze worldwide Global LCD TV Panel market trends, this research provides key statistics on the state of the industry and is a valuable source of guidance and direction for companies and individuals interested in the market.

Large LCD panel prices have been continuously increasing for last 10 months due to an increase in demand and tight supply. This has helped the LCD industry to recover from drastic panel price reductions, revenue and profit loss in 2019. It has also contributed to the growth of QD and miniLED LCD TV. Strong LCD TV panel demand is expected to continue in 2021, but component shortages, supply constraints, and very high panel price increase can still create uncertainties.

It was earlier anticipated that price increases would decelerate in 2Q, but now the price increase is accelerating compared to 1Q, according to a research by DSCC. Panel prices increased by 27 percent in 4Q20 compared to 3Q and slowed down to 14.5 percent in 1Q21 compared to 4Q, but the current estimate is that average LCD TV panel prices in 2Q21 will increase by another 17 percent. The prices are expected to peak sometime in 3Q21.

There has been a surge in prices across the board from a low in May 2020 to a high point in June 2021 which does not represent the peak. There have been multiple inflection points for this cycle: the first inflection point, the month of the biggest MoM price increases, was passed in September 2020, and the price increase slowed down, then started to accelerate again in January 2021, and there is another slowdown starting in May 2021. Prices in May 2021 have reached levels last seen in July 2017.

Prices increased in 1Q21 for all sizes of TV panels, with double-digit percentage increases in sizes from 32- to 65-inch ranging from 12-18 percent. Prices for 75-inch increased by 8 percent as capacity has continued to increase on Gen 10.5 lines, where 75-inch is an efficient six-cut. Prices for every size of TV panel will continue to increase in 2Q at an even faster rate, ranging from 12 percent for 75-inch to 24 percent for 32-inch. The prices are expected to continue to increase in 3Q.

The current upturn in the crystal cycle has seen the biggest trough-to-peak price increases for LCD TV panels, and the recent acceleration of prices has further extended this record. Comparing the forecast for June 2021 panel prices with the prices in May 2020, there is a trough-to-peak increases from 34 percent for 75-inch to 181 percent for 32-inch, with an average of 111 percent. In comparison, the average trough-to-peak increase of the 2016 to 2017 cycle was 48 percent, and prior cycles saw smaller increases.

Before the current upswing, the largest panels sold with an area premium, but the current cycle has flipped that upside down. Whereas in May 2020, 75-inch panels sold at an area premium of USD 77 per square meter higher than the 32-inch panel price, as of May 2021, they are selling at a USD 65 discount on an area basis. This means that those Gen 10.5 fabs could earn higher revenues from making 32-inch panels than from 75-inch panels. The pattern for 65-inch is even more severe, and 65-inch is now selling at a USD 69 per square meter discount (alternately, a 22% area discount) compared to 32-inch.

The improved pricing for LCD TV panels has already improved the profitability of panel makers. It will continue to drive their profits even higher, especially the two prominent Taiwanese players, who have Gen 7.5 and Gen 8.5 fabs but no Gen 10.5 fabs. Chinese panel makers HKC and CHOT have a similar industrial profile and stand to benefit greatly as well. The leading companies with Gen 10.5 fabs (BOE, CSOT and Foxconn/Sharp) stand to benefit less because the price increases on the largest sizes are more modest, but every LCD panel maker is doing well.

In addition to being an exceptionally large upcycle, the current upswing matches some of the longest stretches of increasing prices ever seen, more than a full year from trough to peak. The length of the upswing can be attributed to several factors: glass and driver IC shortages, the pandemic-driven demand or the potential for Korean fab downsizing.

TV makers continued to make strong profits in 1Q21 despite increasing panel prices. The TV market typically slows down in 1Q and 2Q. TV maker revenues declined seasonally in 1Q but less than usual, and the operating margins for both Samsung and LGE increased sequentially. Samsung’s CE division operating profits exceeded USD 1 billion for the quarter for only the second time ever. With demand remaining strong, TV makers have weathered the increase in panel prices and remained very profitable.

There is a surge in LCD equipment spending to respond to dramatically improved market conditions in the LCD market. DSCC sees LCD revenues rising 32 percent in 2021 to USD 112 billion on strong unit and area growth with prices and profitability rebounding to or even exceeding the 2017 levels. With LCD suppliers able to sell everything they can make at attractive margins; it should be no surprise that most LCD manufacturers are looking to expand capacity.

However, unlike previous upturns when many new fabs were built, in this upturn panel suppliers are looking to stretch their capacity through smaller investments, simplifying their processes and debottlenecking. Having said that, there will be two new Gen 8.6 mega fabs being built. The result versus last quarter is a 10 percent or a USD 2.2 billion increase in 2020-2024 LCD spending from USD 21.8 billion to USD 24 billion. The 2021 LCD equipment spending forecast is up 15 percent versus last quarter’s forecast to USD 10 billion, with 2021 LCD equipment spending up 125 percent versus 2021. In addition, 2022 was upgraded by 28 percent to USD 3.5 billion.

Although there is a healthy upgrade in LCD equipment spending in 2021 and 2022, the outlook for 2022-2024 spending is still significantly lower than in previous years, resulting in tighter capacity and slower price reductions in the next downturn. In addition, with Korean LCD suppliers expected to reduce their LCD capacity and convert to potentially higher margin OLEDs, the outlook for LCD pricing and profitability looks quite healthy, which may result in even more equipment spending, especially as miniLEDs gain acceptance.

In March 2021 Corning announced its plan to increase glass prices in 2Q21. Corning has also increased supply by starting glass tank in Korea to supply China’s Gen 10.5 fabs that are ramping up. Most of the growth in capacity is coming from Gen 8.6 and Gen 10.5 fabs in China.

Widespread component supply shortages could impact availability on LCD TV panels from CSOT and Innolux. The display panel manufacturers have warned that supplies of panels are expected to be tight throughout the year.

According to Li Dongsheng, chairman, TCL, panel shortages will continue in 1H21, following conditions already hampered last year during the start of the COVID-19 pandemic. The situation for 2H21 remains to be seen but for 2021 overall panel supply will be tight.

James Yang, president, Innolux, has warned of a shortage in LCD panels caused by strong demand for LCD coming out of the global crisis and the conditions are expected to continue through 2021. Innolux has seen shortages in LCD components including power semiconductors, driver ICs and glass substrates that have kept production below capacity. Shortages of ICs and semiconductors could continue right up to the 1H22.

Ironically, prior to the run-on LCD panel supplies, manufacturers were faced with the dilemma of overproduction causing a glut in inventory, which was driving prices artificially lower. This was the result of giant new LCD fabs coming online in China and other areas of Asia.

Panel makers, being cognizant of that threat, are expected to produce panels at a more tempered pace to keep margins healthy. LCD panel prices continued to rise in March after moving up in February.

Almost all Chinese panel makers are doing everything they can to incrementally increase their current factories’ capacities through productivity enhancements and new equipment purchases for debottlenecking or capacity expansions. For the same reasons, South Korean panel makers continue to delay shutting down their domestic LCD TV factories.

TV manufacturers have been moving aggressively to replenish inventories of LCD panels to meet strong sales of TVs and other devices to meeting escalating demand, particularly in the United States and Europe.

An increase in demand for larger size TVs in 2H20 combined with component shortages has pushed the market to supply constraint and caused continuous panel price increases from June 2020 to March 2021. The panel price increase resulting in higher costs for TV brands. It has also made it difficult for lower priced brands to acquire enough panels to offer lower priced TVs. Further, panel suppliers are giving priority to top brands with larger orders during supply constraint.

For 3 years, from 2017 to 2020, LCD panel makers suffered through a continuous pattern of price declines interrupted only with brief respites. With the COVID-19 demand surge assisted by shortages in glass and DDICs, panel prices are spiking. Korean, Taiwanese, and Chinese panel makers are reporting robust margins in 1Q 2021 and the good news is anticipated for panel makers to get even better in 2Q.

Although multiple caveats remain about how both supply and demand will trend over the coming months, the modeled glut level is a leading indicator that the next cycle is now on its way, which implies falling prices, utilization, and profitability. Industry players should consider the implications when planning business strategies for the next 2 years.

Flat-panel displays are thin panels of glass or plastic used for electronically displaying text, images, or video. Liquid crystal displays (LCD), OLED (organic light emitting diode) and microLED displays are not quite the same; since LCD uses a liquid crystal that reacts to an electric current blocking light or allowing it to pass through the panel, whereas OLED/microLED displays consist of electroluminescent organic/inorganic materials that generate light when a current is passed through the material. LCD, OLED and microLED displays are driven using LTPS, IGZO, LTPO, and A-Si TFT transistor technologies as their backplane using ITO to supply current to the transistors and in turn to the liquid crystal or electroluminescent material. Segment and passive OLED and LCD displays do not use a backplane but use indium tin oxide (ITO), a transparent conductive material, to pass current to the electroluminescent material or liquid crystal. In LCDs, there is an even layer of liquid crystal throughout the panel whereas an OLED display has the electroluminescent material only where it is meant to light up. OLEDs, LCDs and microLEDs can be made flexible and transparent, but LCDs require a backlight because they cannot emit light on their own like OLEDs and microLEDs.

Liquid-crystal display (or LCD) is a thin, flat panel used for electronically displaying information such as text, images, and moving pictures. They are usually made of glass but they can also be made out of plastic. Some manufacturers make transparent LCD panels and special sequential color segment LCDs that have higher than usual refresh rates and an RGB backlight. The backlight is synchronized with the display so that the colors will show up as needed. The list of LCD manufacturers:

Organic light emitting diode (or OLED displays) is a thin, flat panel made of glass or plastic used for electronically displaying information such as text, images, and moving pictures. OLED panels can also take the shape of a light panel, where red, green and blue light emitting materials are stacked to create a white light panel. OLED displays can also be made transparent and/or flexible and these transparent panels are available on the market and are widely used in smartphones with under-display optical fingerprint sensors. LCD and OLED displays are available in different shapes, the most prominent of which is a circular display, which is used in smartwatches. The list of OLED display manufacturers:

MicroLED displays is an emerging flat-panel display technology consisting of arrays of microscopic LEDs forming the individual pixel elements. Like OLED, microLED offers infinite contrast ratio, but unlike OLED, microLED is immune to screen burn-in, and consumes less power while having higher light output, as it uses LEDs instead of organic electroluminescent materials, The list of MicroLED display manufacturers:

LCDs are made in a glass substrate. For OLED, the substrate can also be plastic. The size of the substrates are specified in generations, with each generation using a larger substrate. For example, a 4th generation substrate is larger in size than a 3rd generation substrate. A larger substrate allows for more panels to be cut from a single substrate, or for larger panels to be made, akin to increasing wafer sizes in the semiconductor industry.

"Samsung Display has halted local Gen-8 LCD lines: sources". THE ELEC, Korea Electronics Industry Media. August 16, 2019. Archived from the original on April 3, 2020. Retrieved December 18, 2019.

"TCL to Build World"s Largest Gen 11 LCD Panel Factory". www.businesswire.com. May 19, 2016. Archived from the original on April 2, 2018. Retrieved April 1, 2018.

"Panel Manufacturers Start to Operate Their New 8th Generation LCD Lines". 대한민국 IT포털의 중심! 이티뉴스. June 19, 2017. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"TCL"s Panel Manufacturer CSOT Commences Production of High Generation Panel Modules". www.businesswire.com. June 14, 2018. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"Samsung Display Considering Halting Some LCD Production Lines". 비즈니스코리아 - BusinessKorea. August 16, 2019. Archived from the original on April 5, 2020. Retrieved December 19, 2019.

Herald, The Korea (July 6, 2016). "Samsung Display accelerates transition from LCD to OLED". www.koreaherald.com. Archived from the original on April 1, 2018. Retrieved April 1, 2018.

www.etnews.com (30 June 2017). "Samsung Display to Construct World"s Biggest OLED Plant". Archived from the original on 2019-06-09. Retrieved 2019-06-09.

"China"s BOE to have world"s largest TFT-LCD+AMOLED capacity in 2019". ihsmarkit.com. 2017-03-22. Archived from the original on 2019-08-16. Retrieved 2019-08-17.

A major decrease in manufacturing cost gap between organic light-emitting diode (OLED) display and liquid crystal display (LCD) panel is expected to support the expansion of OLED TVs, according to new analysis from IHS Markit (Nasdaq: INFO).

The OLED Display Cost Modelanalysis estimates that the total manufacturing cost of a 55-inch OLED ultra-high definition (UHD) TV panel — at the larger end for OLED TVs — stood at $582 per unit in the second quarter of 2017, a 55 percent drop from when it was first introduced in the first quarter of 2015. The cost is expected to decline further to $242 by the first quarter of 2021, IHS Markit said.

The manufacturing cost of a 55-inch OLED UHD TV panel has narrowed to 2.5 times that of an LCD TV panel with the same specifications, compared to 4.3 times back in the first quarter of 2015.

“Historically, a new technology takes off when the cost gap between a dominant technology and a new technology gets narrower,” said Jimmy Kim, principal analyst for display materials at IHS Markit. “The narrower gap in the manufacturing cost between the OLED and LCD panel will help the expansion of OLED TVs.”

However, it is not just the material that determines the cost gap. In fact, when the 55-inch UHD OLED TV panel costs were 2.5 times more than LCD TV panel, the gap in the material costs was just 1.7 times. Factors other than direct material costs, such as production yield, utilization rate, depreciation expenses and substrate size, do actually matter, IHS Markit said.

The total manufacturing cost difference will be reduced to 1.8 times from the current 2.5 times, when the yield is increased to a level similar to that of LCD panels. “However, due to the depreciation cost of OLED, there are limitations in cost reduction from just improving yield,” Kim said. “When the depreciation is completed, a 31 percent reduction in cost can be expected from now.”

LCD TV Panel Market Size is projected to Reach Multimillion USD by 2028, In comparison to 2021, at unexpected CAGR during the forecast Period 2022-2028.

This research report is the result of an extensive primary and secondary research effort into the LCD TV Panel market. It provides a thorough overview of the market"s current and future objectives, along with a competitive analysis of the industry, broken down by application, type and regional trends. It also provides a dashboard overview of the past and present performance of leading companies. A variety of methodologies and analyses are used in the research to ensure accurate and comprehensive information about the LCD TV Panel Market.

The Global LCD TV Panel market is anticipated to rise at a considerable rate during the forecast period, between 2023 and 2028. In 2021, the market is growing at a steady rate and with the rising adoption of strategies by key players, the market is expected to rise over the projected horizon.

LCD displays utilize two sheets of polarizing material with a liquid crystal solution between them. An electric current passed through the liquid causes the crystals to align so that light cannot pass through them. Each crystal, therefore, is like a shutter, either allowing light to pass through or blocking the light. LCD panel is the key components of LCD display. And the price trends of LCD panel directly affect the price of liquid crystal displays. LCD panel consists of several components: Glass substrate, drive electronics, polarizers, color filters etc. Only LCD panel applied for TV will be counted in this report.

Due to the COVID-19 pandemic, the global LCD TV Panel market size is estimated to be worth USD 54770 million in 2022 and is forecast to a readjusted size of USD 62410 million by 2028 with a CAGR of 2.2% during the forecast period 2022-2028. Fully considering the economic change by this health crisis, 32"" and Below accounting for % of the LCD TV Panel global market in 2021, is projected to value USD million by 2028, growing at a revised % CAGR from 2022 to 2028. While Residential segment is altered to an % CAGR throughout this forecast period.

Global LCD TV Panel key players include Samsung Display, LG Display, Innolux Crop, AUO, CSOT, etc. Global top five manufacturers hold a share over 80%.

The research report has incorporated the analysis of different factors that augment the marketâs growth. It constitutes trends, restraints, and drivers that transform the market in either a positive or negative manner. This section also provides the scope of different segments and applications that can potentially influence the market in the future. The detailed information is based on current trends and historic milestones. This section also provides an analysis of the volume of production about the global market and about each type from 2017 to 2028. This section mentions the volume of production by region from 2017 to 2028. Pricing analysis is included in the report according to each type from the year 2017 to 2028, manufacturer from 2017 to 2022, region from 2017 to 2022, and global price from 2017 to 2028.

The research report includes specific segments by region (country), by manufacturers, by Size and by Application. Each type provides information about the production during the forecast period of 2017 to 2028. by Application segment also provides consumption during the forecast period of 2017 to 2028. Understanding the segments helps in identifying the importance of different factors that aid the market growth.

This LCD TV Panel Market Research/Analysis Report Contains Answers to your following Questions ● What are the global trends in the LCD TV Panel market? Would the market witness an increase or decline in the demand in the coming years?

● What is the estimated demand for different types of products in LCD TV Panel? What are the upcoming industry applications and trends for LCD TV Panel market?

● What Are Projections of Global LCD TV Panel Industry Considering Capacity, Production and Production Value? What Will Be the Estimation of Cost and Profit? What Will Be Market Share, Supply and Consumption? What about Import and Export?

● How big is the opportunity for the LCD TV Panel market? How will the increasing adoption of LCD TV Panel for mining impact the growth rate of the overall market?

Browse Market Size, charts, tables and figures extent in-depth TOC with 97 Report Pages on Plasma Display Panel Market by Application (Plasma TV, Seamless Video Wall, Others), by Type (Small Size Display Below 42 Inch, Middle Size Display 42-51 Inch, Large Size Display Above 51 Inch) Business Outlook, Top Companies, Key Regions, Product Demand, Market Size and Growth.

Plasma Display Panel market focuses on analyzing the current competitive situation in the Plasma Display Panel market and provides basic information, market data, product introductions, etc. of leading companies in the industry. At the same time, includes the highlighted analysis--Strategies for Company to Deal with the Impact of COVID-19, It may also be helpful to consult with a financial who can provide direction based on your specific financial situation and goals.

Plasma display panels (PDP) are a ï¬at panel display technology that uses small cells containing electrically charged ionized gases, or plasmas, to produce an image. A plasma display consists of millions of tiny gas-filled compartments, or cells, between two panels of glass.

This technology came out as a concept by a Hungarian engineer in 1936. Until 1992, Fujitsu introduced the world"s first 21-inch (53 cm) full-color display. After around 2 decadesâ commercialization, PDP used to be a strong competitor to CRT and LCD panel.

With the advantage such as: capable of producing deeper blacks allowing for superior contrast ratio; wider viewing angles than those of LCD; less visible motion blur; less expensive for the buyer per square inch than LCD, PDP used to have a very strong marketing drive. But also with the significant disadvantages: screen burn-in and image retention; panel couldnât be cut small as LCD can, also heavier than those coming display advance products like LCD, LED, OLED. When Samsung and Changhong LTD announced halt the panel production in 2014, plasma display panel walked out the stage of history.

Due to the COVID-19 pandemic, the global Plasma Display Panel market size is estimated to be worth USD million in 2022 and is forecast to a readjusted size of USD million by 2028 with a CAGR of % during the review period. Fully considering the economic change by this health crisis, Small Size Display Below 42 Inch accounting for % of the Plasma Display Panel global market in 2021, is projected to value USD million by 2028, growing at a revised % CAGR in the post-COVID-19 period. While Plasma TV segment is altered to an % CAGR throughout this forecast period.

In terms of production side, this report researches the Plasma Display Panel capacity, production, growth rate, market share by manufacturers and by region (region level and country level), from 2017 to 2022, and forecast to 2028.

In terms of sales side, this report focuses on the sales of Plasma Display Panel by region (region level and country level), by company, by Size and by Application. from 2017 to 2022 and forecast to 2028.

Plasma Display Panel market is segmented by Size and by Application. Players, stakeholders, and other participants in the global Plasma Display Panel market will be able to gain the upper hand as they use the report as a powerful resource. The segmental analysis focuses on production capacity, revenue and forecast by Size and by Application for the period 2017-2028.

This study also covers company profiling, specifications and product picture, sales, market share and contact information of various regional, international and local vendors of Plasma Display Panel Market. The market proposition is frequently developing ahead with the rise in scientific innovation and MandA activities in the industry. Additionally, many local and regional vendors are offering specific application products for varied end-users. The new merchant applicants in the market are finding it hard to compete with the international vendors based on reliability, quality and modernism in technology.

â Comprehensive valuation of all prospects and threat in the â In depth study of industry strategies for growth of the Plasma Display Panel market-leading players.

(Yicai Global) June 13 -- BOE Technology Group, TCL China Star Optoelectronics Technology and other big Chinese liquid crystal display manufacturers are reducing output starting from this month to try and stop a freefall in prices caused by a global glut.

Panel makers are cutting production by 16 percent on average from this month, Rong Chaoping, senior researcher at market research firm AVC Revo, told Yicai Global. Television panel makers are expected to ship 3.6 million less panels than last month.

Panel makers will reduce capacity by between 15 and 20 percent this month, said Wu Rongbing, chief analyst at Chinese semiconductor intelligence service Omdia.

LCD TV display shipments from China’s five largest panel manufacturers accounted for 68.5 percent of the global market in April, a new high, and they were expected to exceed 70 percent this year, according to Omdia.

But there is much less demand for notebook computers, monitors and TVs now that fewer people are working from home as the Covid-19 pandemic wanes and amid pressure from global inflation. This is driving prices down, said Li Yaqin, general manager of market research firm Sigmaintell.

The global panel industry is expected to slash production by about 20 percent this year, according to Beijing-based Sigmaintell. It is the first time since 2013 that the worldwide sector has implemented such a large-scale and wide-ranging cut in manufacturing. But it should help to slow the fall in prices, Li said.

“Tumbling prices are squeezing profits,” Li said. “The price of a TV panel is now below cost price and that of some data panels is also below the manufacturing cost.”

“Panel makers are facing rising liquidity pressure and bigger losses as prices are now below cost price, so the display industry is likely to undergo another big reshuffle,” Rong said.

Excess supply will ease in the third quarter once output is cut, and prices will start to pick up and then flatten out, Li said. Demand for consumer electronic products is shrinking by far more than expected so it is too early to tell whether prices will rebound in the second half, she added.

Panel prices are likely to stop dropping this month or next as output falls, Wu said. Whether prices will start to pick up soon depends on when demand improves.

LCD TV panel prices have reached all-time lows but they continue to decline, and although the pace of decline is slowing in the third quarter, we now forecast that the industry will have an “L-shaped” recovery in the fourth quarter. In other words, no recovery at all until 2023. The ‘perfect storm’ of a continued oversupply, near-universally weak demand and excessive inventory throughout the supply chain has combined, and every screen size of TV panel has reached an all-time low price. Although fab utilization has slowed sharply in July, we do not see any signal to suggest that prices can increase any time soon.

LG Display and Samsung Display are struggling to find their ways out of the deterioration of their performance even after withdrawing from production of liquid crystal display (LCD) panels. The high-priced organic light emitting diode (OLED) panel sector regarded as a future growth engine is not growing fast due to the economic downturn. Even in the OLED panel sector, Chinese display makers are within striking distance of Korean display makers, experts say.

On Aug. 30, Display Supply Chain Consultants (DSCC), a market research company, predicted that LCD TV panel prices hit an all-time low in August and that an L-shaped recession will continue in the fourth quarter. According to DSCC, the average price of a 65-inch ultra-high-definition (UHD) panel in August was only US$109, a 62 percent drop from the highest price of US$288 recorded in July in 2021. The average price of a 75-inch UHD panel was only US$218, which was only about half of the highest price of US$410 in July last year. DSCC predicted that the average panel price in the third quarter will fall by 15.7 percent. As Chinese companies’ price war and the effect of stagnation in consumption overlapped, the more LCD panels display makers produce, the more loss they suffer.

As panel prices fell, manufacturers responded by lowering facility utilization rates. DSCC said that the LCD factory utilization rate descended from 87 percent in April to 83 percent in May, 73 percent in June, and 70 percent in July.

Now that the LCD panel business has become no longer lucrative, Korean display makers have shut down their LCD business or shrunk their sizes. In the LCD sector, China has outpaced Korea since 2018. China’s LCD market share reached 50.9 percent in 2021, while that of Korea dropped to 14.4 percent, lower than Taiwan’s 31.6 percent.

Samsung Display already announced its withdrawal from the LCD business in June. Only 10 years have passed since the company was spun off from Samsung Electronics in 2012. LG Display has decided to halt domestic LCD TV panel production until 2023 and reorganize its business structure centering on OLED panels. Its Chinese LCD production line will be gradually converted to produce LCD panels for IT or commercial products. TrendForce predicted that LG Display will stop operating its P7 Plant in the first quarter of next year.

Korean display makers’ waning LCD business led to a situation in which Korea even lost first place in the display industry. Korea with a display market share of 33.2 percent was already overtaken by China with 41.5 percent) in 2021 according to market researcher Omdia and the Korea Display Industry Association. Korea’s market share has never rebounded in for five years since 2017 amid the Korean government’s neglect. Seventeen years have passed since 2004 when Korea overtook Japan to rise to the top of the world in the LCD industry. Korea’s LCD exports amounted to more than US$30 billion in 2014, but fell to US$21.4 billion last year.

A bigger problem is that Korean display makers may lose its leadership in the OLED panel sector although it is still standing at the top spot. While Korea’s OLED market share fell from 98.1 percent in 2016 to 82.8 percent last year, that of China rose from 1.1 percent to 16.6 percent. Considering that the high-end TV market is highly likely to shrink for the time being due to a full-fledged global consumption contraction, some analysts say that the technology gap between Korea and China can be sharply narrowed through this looming TV market slump. According to industry sources, the Chinese government is now focusing on giving subsidies to the development of OLED panel technology rather LCD technology. On the other hand, in Korea, displays were also wiped out from national strategic technology industry items under the Restriction of Special Taxation Act which can receive tax benefits for R&D activities on displays.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey