lcd panel production cost manufacturer

LCD panel prices have risen for 4 months in a row because of your home gaming? Since this year, the whole LCD panel market has smoked. Whether after the outbreak of the epidemic, LCD panel market prices rose for four months, or the panel giants in Japan and South Korea successively sold production lines, or the Chinese mainland listed companies frequently integrated acquisition, investment, and plant construction, all make the industry full of interesting.

LCD panel prices are already a fact. Since May this year, LCD panel prices have risen for four months in a row, making the whole industry chain dynamic. Why are LCD panels going up in price in a volatile 2020? The key factor lies in the imbalance between supply and demand.

The price of LCDS for large-size TVs of 70 inches or more hasn’t budged much. In addition, LTPS screens and AMOLED screens used in high-end phones have seen little or no increase in price.

As for October, LCD panel price increases are expected to moderate. The data shows that in October 32 inches or 2 dollars; Gains of 39.5 to 43 inches will shrink to $3;55 inches will fall back below $10; The 65-inch gain will narrow to $5.

During the epidemic, people stayed at home and had no way to go out for entertainment. They relied on TV sets, PCS, and game consoles for entertainment. After the resumption of economic work and production, the market of traditional home appliances picked up rapidly, and LCD production capacity was quickly digested.

However, due to the shutdown of most factories lasting 1-2 months during the epidemic period, LCD panel production capacity was limited, leading to insufficient production capacity in the face of the market outbreak, which eventually led to the market shortage and price increase for 4 consecutive months.

In fact, the last round of price rise of LCD panels was from 2016 to 2017, and its overall market price has continued to fall since 2018. Even in 2019, individual types have fallen below the material cost, and the whole industry has experienced a general operating loss. As a result, LCD makers have been looking for ways to improve margins since last year.

A return to a reasonable price range is the most talked about topic among panel makers in 2019, according to one practitioner. Some manufacturers for the serious loss of the product made the decision to reduce production or even stop production; Some manufacturers planned to raise the price, but due to the epidemic in 2020, the downstream demand was temporarily suppressed and the price increase was postponed. After the outbreak was contained in April, LCD prices began to rise in mid-to-late May.

In fact, the market price of LCD panels continued to decline in 2018-2019 because of the accelerated rise of China’s LCD industry and the influx of a large number of local manufacturers, which doubled the global LCD panel production capacity within a few years, but there was no suitable application market to absorb it. The result of excess capacity is oversupply, ultimately making LCD panel prices remain depressed.

Against this background, combined with the impact of the epidemic in 2020, the operating burden of LCD companies in Japan and South Korea has been further aggravated, and it is difficult to make profits in the production of LCD panels, so they have to announce the withdrawal of LCD business.

business in June 2022. In August, Sharp bought JDI Baishan, a plant in Ishikawa prefecture that makes liquid crystal display panels for smartphones. In early September, Samsung Display sold a majority stake in its SUZHOU LCD production plant to Starlight Electronics Technology, a unit of TCL Technology Group. LGD has not only pulled out of some of its production capacity but has announced that it will close its local production line in 2020. According to DSCC, a consultancy, the share of LCD production capacity in South Korea alone will fall from 19% to 7% between 2020 and 2021.

It is worth mentioning that in industry analysis, in view of the fact that Korean companies are good at using “dig through old bonus – selling high price – the development of new technology” the cycle of development mode, another 2020 out of the LCD production capacity, the main reason may be: taking the advantage of China’s expanding aggressively LCD manufacturers, Korean companies will own LCD panel production line hot sell, eliminating capacity liquid to extract its final value, and turning to the more profitable advantage of a new generation of display technologies, such as thinner, color display better OLED, etc. Samsung, for example, has captured more than 80% of the OLED market with its first-mover advantage.

From the perspective of production capacity, the launch of LCD tracks by major manufacturers in Japan and South Korea must reduce some production capacity in the short term, which to some extent induces market price fluctuations. In the long run, some of the Japanese and Korean LCD production capacity has been bought by Chinese manufacturers, coupled with frequent investment in recent years, the overall capacity is sure to recover as before, or even more than before. But now it will take time to expand the production layout, which more or less will cause supply imbalance, the industry needs to be cautious.

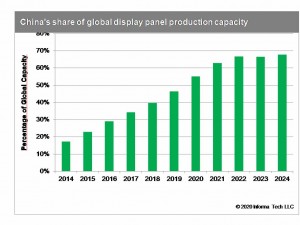

The LCD panel industry started in the United States and then gradually moved to Japan, South Korea, China, and Taiwan. At present, the proportion of production capacity in The Chinese mainland has reached 52% in 2020, and there are leading LCD panel products in China represented by BOE, Huxing Optoelectronics. Meanwhile, the production capacity layout of BOE, Huike, Huxing Optoelectronics, and other manufacturers has been basically completed, making industrial integration a necessity.

On the one hand, South Korean enterprises out of the LCD track, the domestic factory horse enclosure, plant expansion action. While LCDs may not sell as well as “upstart” flexible screens, respondents believe they are still strong enough in the traditional home appliance market to warrant continued investment. Zhao Bin, general manager of TCL Huaxing Development Center, has said publicly that the next-generation display technology will be mature in four to five years, but the commercialization of products may not take place until a decade later. “LCD will still be the mainstream in this decade,” he said.

On the other hand, there is no risk of neck jam in China’s LCD panel industry, which is generally controllable. In mainland China, there will be 21 production lines capable of producing 32-inch or larger LCD panels by 2021, accounting for about two-thirds of the global total. In terms of the proportion of production capacity, the Chinese mainland accounted for 42% of the global LCD panel in 2019, 51% this year, and will continue to climb to 63% next year.

Of course, building factories and expanding production cannot be accomplished overnight. In the process of production capacity recovery, it is predicted that there will be several price fluctuations, and the cost may be passed on to the downstream LCD panel manufacturers or consumers when the price rises greatly, which requires continuous attention.

According to the OLED Display Cost Model by IHS Markit, manufacturing cost of the 5.9-inch organic light-emitting diode (OLED) panel with notch design, as in the Apple iPhone X, is estimated to be $29. It is found to be 25 percent higher than manufacturing cost of full-display OLED panel without the notch design used in the 5.8-inch display for the Samsung Galaxy S9. Similar cost gap is also found in the thin-film transistor liquid crystal display (TFT-LCD). Manufacturing cost of a 6-inch notch TFT-LCD panel is estimated to be $19, 20 percent higher than similar-sized non-notch, full-display LCD panel.

“Notch cutting should accompany yield loss, resulting in increases in manufacturing cost. In case of TFT-LCD, a notch design may push up the manufacturing cost even to the level of rigid, full-screen OLED’s,” said Jimmy Kim, Ph.D. and senior principal analyst for display materials at IHS Markit. “For OLED panels, cost increase caused by notch design seems to be even higher.”

Quarterly shipments of the iPhone X, Apple’s first smartphone model using OLED panels, have reportedly been smaller than previous iPhone models’ so far, mainly due to higher selling price, caused by expensive OLED panels. “Apple seems to be in the middle of manufacturing optimization,” Kim said.

“Eventually, manufacturing cost for notch OLED will fall more rapidly than that for notch TFT-LCD. The plastic substrate for OLED is not as brittle as glass used in TFT-LCD, so it should be easier to cut the notch, theoretically.”

The OLED Display Cost Model by IHS Markit includes manufacturing cost analysis and forecasts of OLED display panels in mass production for smartwatch, smartphone, tablet PC and TV.

Once it’s recognized that a custom display will be a better design and lead to a lower overall system-level cost it’s time to dive into the actual tooling costs.

Semi-custom is typically the preferred option to start with. And in the case of color TFT, it’s typically the only option, as the TFT panel comes with a significant tooling and minimum order quantity (MOQ) such that the customization costs outweigh the drawbacks of using the closest standard TFT glass platform available.

b) Custom color TFT displays— the bulk of this cost comes from the TFT glass cell at $70K–$200K depending on the type of TFT cell used (standard TN or IPS). The balance of the module is an additional $5,000 – $15,000.

f) Touch panels— resistive touch panels cost approximately $2,500, while capacitive touch panels can range between $4,000 and $10,000. If a standard capacitive touch sensor can be used, and only a custom top surface is customized, the tooling can be reduced to only $1,500.

Now that we’ve reviewed some of the costs associated with custom displays, here are some tips you can use to make sure that you move forward with the right partner that will then support this custom display for the long term.

Many LCD display manufacturers try to accommodate all order volumes they receive. While this allows them to serve a wider range of customers, it makes them less specialized for serving certain types of customers. As a result, your specific production volumes may be prohibitively expensive.

Seek out a display manufacturer who is optimized to handle your specific production needs for LCD displays. This is necessary to get the display for the right cost and the appropriate level of support.

Always start with a semi-custom approach. Use the available standard products to base the new design on, and then keep modifying as needed. This results in the lowest tooling costs and an easier design process. And in the case of color TFT, unless you are developing the next iPhone, design your display based on one of the standard glass platforms readily available. Then from there, redesign the backlight and the mechanical and electrical interface for your specific application.

Behind every great company are happy customers. Find out whether your supplier has them. Make sure that when this experience is handed off from your supplier’s sales and design team, the production team is just as good and accommodating. This can be accomplished through references and audits.

BOE Technology Group, the Chinese electronic components producer, is expected to be the leader in producing LCD display panels in the coming years, with a forecast capacity share of 24 percent by 2022. China is the country that has the largest LCD capacity, with a 56 percent share in 2020.Read moreLCD panel production capacity share from 2016 to 2022, by manufacturerCharacteristicBOEChina StarInnoluxAUOLGDHKCCEC PandaSharpSDCOther-----------

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2022, by manufacturer [Graph]. In Statista. Retrieved January 07, 2023, from https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "LCD panel production capacity share from 2016 to 2022, by manufacturer." Chart. June 8, 2020. Statista. Accessed January 07, 2023. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. (2020). LCD panel production capacity share from 2016 to 2022, by manufacturer. Statista. Statista Inc.. Accessed: January 07, 2023. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2022, by Manufacturer." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC, LCD panel production capacity share from 2016 to 2022, by manufacturer Statista, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/ (last visited January 07, 2023)

The statistic shows the manufacturing cost of a 55-inch ultra-high definition (UHD) TV panel from the first quarter of 2015 to the second quarter of 2017, broken down by technology. In the first quarter of 2017, the manufacturing cost of a 55-inch OLED UHD TV panel amounted to around 600 U.S. dollars per unit.Read moreManufacturing cost of a 55-inch UHD TV panel from 1st quarter 2015 to 2nd quarter 2017 (in U.S. dollars), by technologyCharacteristicLCDOLED---

Statista. (March 1, 2018). Manufacturing cost of a 55-inch UHD TV panel from 1st quarter 2015 to 2nd quarter 2017 (in U.S. dollars), by technology [Graph]. In Statista. Retrieved January 07, 2023, from https://www.statista.com/statistics/784279/55-inch-uhd-tv-panel-manufacturing-cost-by-technology/

Statista. "Manufacturing cost of a 55-inch UHD TV panel from 1st quarter 2015 to 2nd quarter 2017 (in U.S. dollars), by technology." Chart. March 1, 2018. Statista. Accessed January 07, 2023. https://www.statista.com/statistics/784279/55-inch-uhd-tv-panel-manufacturing-cost-by-technology/

Statista. (2018). Manufacturing cost of a 55-inch UHD TV panel from 1st quarter 2015 to 2nd quarter 2017 (in U.S. dollars), by technology. Statista. Statista Inc.. Accessed: January 07, 2023. https://www.statista.com/statistics/784279/55-inch-uhd-tv-panel-manufacturing-cost-by-technology/

Statista. "Manufacturing Cost of a 55-inch Uhd Tv Panel from 1st Quarter 2015 to 2nd Quarter 2017 (in U.S. Dollars), by Technology." Statista, Statista Inc., 1 Mar 2018, https://www.statista.com/statistics/784279/55-inch-uhd-tv-panel-manufacturing-cost-by-technology/

Statista, Manufacturing cost of a 55-inch UHD TV panel from 1st quarter 2015 to 2nd quarter 2017 (in U.S. dollars), by technology Statista, https://www.statista.com/statistics/784279/55-inch-uhd-tv-panel-manufacturing-cost-by-technology/ (last visited January 07, 2023)

For over 20 years we"ve been helping clients worldwide by designing, developing, & manufacturing custom LCD displays, screens, and panels across all industries.

Newhaven Display has extensive experience manufacturing a wide array of digital display products, including TFT, IPS, character displays, graphic displays, LCD modules, COG displays, and LCD panels. Along with these products, we specialize in creating high-quality and affordable custom LCD solutions. While our focus is on high-quality LCD products, we also have a variety of graphic and character OLED displays we manufacture.

As a longtime leader in LCD manufacturing, producing top-quality LCD modules and panels is our highest priority. At Newhaven Display, we’re also incredibly proud to uphold our reputation as a trusted and friendly custom LCD manufacturing company.

As a custom LCD manufacturing company, we ensure complete control of our custom displays" reliability by providing the industry"s highest quality standards. Our design, development, production, and quality engineers work closely to help our clients bring their products to life with a fully custom display solution.

Customer support requests sent by phone, email, or on our support forum will typically receive a response within 24 hours. For custom LCD project inquiries, our response time can take a few days or weeks, depending on the complexity of your display customization requirements. With different production facilities and a robust supply chain, we are able to deliver thefastest turnaround times for display customizations.

Our excellent in-house support and custom display modifications set Newhaven Display apart from other LCD display manufacturers. From TFTs, IPS, sunlight readable displays, HDMI modules, EVE2 modules, to COG, character, and graphic LCDs, our modifications in the customization process are completed at our Illinois facility, allowing us to provide quality and fast turnaround times.

As a display manufacturer, distributor, and wholesaler, we are able to deliver the best quality displays at the best prices. Design, manufacturing, and product assembly are completed at our headquarters in Elgin, Illinois. Newhaven Display International ensures the best quality LCD products in the industry in this newly expanded facility with a renovated production and manufacturing space.

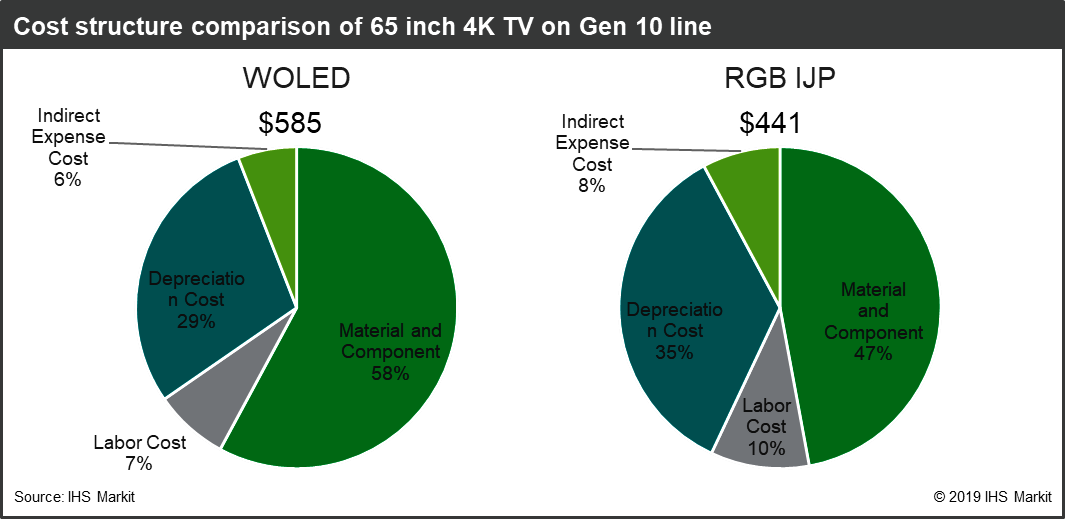

(2 November, 2017) – A major decrease in manufacturing cost gap between organic light-emitting diode (OLED) display and liquid crystal display (LCD) panel is expected to support the expansion of OLED TVs, according to new analysis from

analysis estimates that the total manufacturing cost of a 55-inch OLED ultra-high definition (UHD) TV panel -- at the larger end for OLED TVs -- stood at $582 per unit in the second quarter of 2017, a 55 percent drop from when it was first introduced in the first quarter of 2015. The cost is expected to decline further to $242 by the first quarter of 2021, IHS Markit said.

The manufacturing cost of a 55-inch OLED UHD TV panel has narrowed to 2.5 times that of an LCD TV panel with the same specifications, compared to 4.3 times back in the first quarter of 2015.

“Historically, a new technology takes off when the cost gap between a dominant technology and a new technology gets narrower,” said Jimmy Kim, principal analyst for display materials at IHS Markit. “The narrower gap in the manufacturing cost between the OLED and LCD panel will help the expansion of OLED TVs.”

However, it is not just the material that determines the cost gap. In fact, when the 55-inch UHD OLED TV panel costs were 2.5 times more than LCD TV panel, the gap in the material costs was just 1.7 times. Factors other than direct material costs, such as production yield, utilization rate, depreciation expenses and substrate size, do actually matter, IHS Markit said.

The total manufacturing cost difference will be reduced to 1.8 times from the current 2.5 times, when the yield is increased to a level similar to that of LCD panels. “However, due to the depreciation cost of OLED, there are limitations in cost reduction from just improving yield,” Kim said. “When the depreciation is completed, a 31 percent reduction in cost can be expected from now.”

by IHS Markit provides more detailed cost analysis of OLED panels, including details of boards, arrays, luminescent materials, encapsulants and direct materials such as driver ICs. The report also covers overheads such as occupancy rate, selling, general and depreciation costs. In addition, this report analyzes OLED panels in a wide range of sizes and applications.

New Vision Display is a custom LCD display manufacturer serving OEMs across diverse markets. One of the things that sets us apart from other LCD screen manufacturers is the diversity of products and customizations we offer. Our LCD portfolio ranges from low-cost monochrome LCDs to high-resolution, high-brightness color TFT LCDs – and pretty much everything in between. We also have extensive experience integrating LCD screen displays into complete assemblies with touch and cover lens.

Sunlight readable, ultra-low power, bistable (“paper-like”) LCDs. Automotive grade, wide operating/storage temperatures, and wide viewing angles. Low tooling costs.

Among the many advantages of working with NVD as your LCD screen manufacturer is the extensive technical expertise of our engineering team. From concept to product, our sales and technical staff provide expert recommendations and attentive support to ensure the right solution for your project.

As a leading LCD panel manufacturer, NVD manufactures custom LCD display solutions for a variety of end-user applications: Medical devices, industrial equipment, household appliances, consumer electronics, and many others. Our state-of-the-art LCD factories are equipped to build custom LCDs for optimal performance in even the most challenging environments. Whether your product will be used in the great outdoors or a hospital operating room, we can build the right custom LCD solution for your needs. Learn more about the markets we serve below.

Flat-panel displays are thin panels of glass or plastic used for electronically displaying text, images, or video. Liquid crystal displays (LCD), OLED (organic light emitting diode) and microLED displays are not quite the same; since LCD uses a liquid crystal that reacts to an electric current blocking light or allowing it to pass through the panel, whereas OLED/microLED displays consist of electroluminescent organic/inorganic materials that generate light when a current is passed through the material. LCD, OLED and microLED displays are driven using LTPS, IGZO, LTPO, and A-Si TFT transistor technologies as their backplane using ITO to supply current to the transistors and in turn to the liquid crystal or electroluminescent material. Segment and passive OLED and LCD displays do not use a backplane but use indium tin oxide (ITO), a transparent conductive material, to pass current to the electroluminescent material or liquid crystal. In LCDs, there is an even layer of liquid crystal throughout the panel whereas an OLED display has the electroluminescent material only where it is meant to light up. OLEDs, LCDs and microLEDs can be made flexible and transparent, but LCDs require a backlight because they cannot emit light on their own like OLEDs and microLEDs.

Liquid-crystal display (or LCD) is a thin, flat panel used for electronically displaying information such as text, images, and moving pictures. They are usually made of glass but they can also be made out of plastic. Some manufacturers make transparent LCD panels and special sequential color segment LCDs that have higher than usual refresh rates and an RGB backlight. The backlight is synchronized with the display so that the colors will show up as needed. The list of LCD manufacturers:

Organic light emitting diode (or OLED displays) is a thin, flat panel made of glass or plastic used for electronically displaying information such as text, images, and moving pictures. OLED panels can also take the shape of a light panel, where red, green and blue light emitting materials are stacked to create a white light panel. OLED displays can also be made transparent and/or flexible and these transparent panels are available on the market and are widely used in smartphones with under-display optical fingerprint sensors. LCD and OLED displays are available in different shapes, the most prominent of which is a circular display, which is used in smartwatches. The list of OLED display manufacturers:

MicroLED displays is an emerging flat-panel display technology consisting of arrays of microscopic LEDs forming the individual pixel elements. Like OLED, microLED offers infinite contrast ratio, but unlike OLED, microLED is immune to screen burn-in, and consumes less power while having higher light output, as it uses LEDs instead of organic electroluminescent materials, The list of MicroLED display manufacturers:

LCDs are made in a glass substrate. For OLED, the substrate can also be plastic. The size of the substrates are specified in generations, with each generation using a larger substrate. For example, a 4th generation substrate is larger in size than a 3rd generation substrate. A larger substrate allows for more panels to be cut from a single substrate, or for larger panels to be made, akin to increasing wafer sizes in the semiconductor industry.

"Samsung Display has halted local Gen-8 LCD lines: sources". THE ELEC, Korea Electronics Industry Media. August 16, 2019. Archived from the original on April 3, 2020. Retrieved December 18, 2019.

"TCL to Build World"s Largest Gen 11 LCD Panel Factory". www.businesswire.com. May 19, 2016. Archived from the original on April 2, 2018. Retrieved April 1, 2018.

"Panel Manufacturers Start to Operate Their New 8th Generation LCD Lines". 대한민국 IT포털의 중심! 이티뉴스. June 19, 2017. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"TCL"s Panel Manufacturer CSOT Commences Production of High Generation Panel Modules". www.businesswire.com. June 14, 2018. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"Samsung Display Considering Halting Some LCD Production Lines". 비즈니스코리아 - BusinessKorea. August 16, 2019. Archived from the original on April 5, 2020. Retrieved December 19, 2019.

Herald, The Korea (July 6, 2016). "Samsung Display accelerates transition from LCD to OLED". www.koreaherald.com. Archived from the original on April 1, 2018. Retrieved April 1, 2018.

"China"s BOE to have world"s largest TFT-LCD+AMOLED capacity in 2019". ihsmarkit.com. 2017-03-22. Archived from the original on 2019-08-16. Retrieved 2019-08-17.

Panel makers are cutting production by 16 percent on average from this month, Rong Chaoping, senior researcher at market research firm AVC Revo, told Yicai Global. Television panel makers are expected to ship 3.6 million less panels than last month.

Panel makers will reduce capacity by between 15 and 20 percent this month, said Wu Rongbing, chief analyst at Chinese semiconductor intelligence service Omdia.

TCL China Star intends to continue with its production cuts until September, while Beijing-based BOE and HKC Optoelectronics Technology have not yet decided how long they will reduce output, Rong said. None of the three companies responded when contacted by Yicai Global.

LCD TV display shipments from China’s five largest panel manufacturers accounted for 68.5 percent of the global market in April, a new high, and they were expected to exceed 70 percent this year, according to Omdia.

The global panel industry is expected to slash production by about 20 percent this year, according to Beijing-based Sigmaintell. It is the first time since 2013 that the worldwide sector has implemented such a large-scale and wide-ranging cut in manufacturing. But it should help to slow the fall in prices, Li said.

“Tumbling prices are squeezing profits,” Li said. “The price of a TV panel is now below cost price and that of some data panels is also below the manufacturing cost.”

“Panel makers are facing rising liquidity pressure and bigger losses as prices are now below cost price, so the display industry is likely to undergo another big reshuffle,” Rong said.

Panel prices are likely to stop dropping this month or next as output falls, Wu said. Whether prices will start to pick up soon depends on when demand improves.

After months of price cuts, manufacturers of large-size liquid-crystal displays (LCDs) are under pressure to reduce panel prices further, following a major build-up of inventory. A recent report from US business analyst iSuppli revealed that the second quarter of 2010 saw the manufacture of 52 million large (ten inches and above) LCD television panel shipments, but the sale of only 38.7 million LCD television sets. The resulting imbalance between supply and demand is having a strong impact on the sector.

“This gap is higher than anything seen in 2009. Over-supply persisted in the first two months of the third quarter as buyers cut orders in July and August,” says iSuppli analyst Sweta Dash. “LCD television brands are expected to lower prices more aggressively to reduce their inventory levels, thus putting mounting pressure on panel suppliers to reduce prices further.”

Dash points out that manufacturers of monitor and notebook panels have been reducing supply to mitigate excessive inventory levels, and that panel prices are now stabilizing as a result. In contrast, high depreciation costs at relatively new LCD television panel fabrication plants mean suppliers have been less willing to reduce production.

However, Dash predicts that the potentially strong sales of LCD television sets in China could reduce inventory levels and help to steady panel prices by the end of the fourth quarter of 2010.

At the same time, rapidly rising sales of smart phones and tablet PCs are predicted to see the global market for small- and medium-size thin-film transistor (TFT) LCDs expanding at its fastest pace for three years. According to analyst Vinita Jakhanwal, also from iSuppli, global shipments of TFT LCD panels are set to rise by 28.1% in 2010, from 1.8 billion to 2.3 billion units.

“Sales of smart phones and tablets are booming thanks to the iPhone, iPad and other competing products,” explains Jakhanwal. “Smart phone manufacturers are now adopting TFT LCDs that use in-plane switching technology, which supports a wider viewing angle and better picture quality than a conventional LCD.” But the fast-paced market expansion probably won"t last, predicts Jakhanwal. “Growth in TFT LCD shipments will slow in 2011 and beyond as the expansion of smart phone and tablet markets cools to more normal levels.”

AMOLED technology rose in popularity after its integration into mobile phones manufactured by Samsung and HTC. In the first quarter of 2010, the average screen size for an AMOLED display exceeded three inches, which is larger than that of competing TFT LCDs. Taiwan-based display manufacturers AUO and Chimei Innolux are scheduled to start mass-producing AMOLED displays in 2011. Hsieh believes AMOLED technology will now see increased year-on-year growth, although TFT LCDs will still ship more units.

Flat panel displays use different backplane technologies. Small and medium OLEDs for mobile phones use a low temperature polysilicon (LTPS) backplane which is created by laser annealing amorphous silicon (a-Si). OLED TVs use a metal oxide backplane. Both backplanes use deposited thin films which must be highly uniform and contamination free to maximize electrical performance. The OLEDs are evaporated or deposited and encapsulated to reduce degradation caused by water vapor and oxygen exposure. Encapsulation uses either strengthened glass or thin films, depending on whether the OLED is rigid or flexible. Dissimilarity of materials within the rigid and flexible stacks make cutting and singulation of individual display devices a challenge. The highly complex nature of this process can induce defects, decreasing throughput and yield.

A few India-based enterprises have decided or plan to set up display panel plants in India, but this is unlikely to have substantially impact on the existing global display supply chain in the foreseeable future, as the total panel production capacity in India will be much smaller than that in China, South Korea, Taiwan and Japan.

Under the Indian government"s Production Linked Incentive (PLI) scheme, Elest, a subsidiary of India-based Rajesh Exports - which is among the globally top-500 enterprises - will invest INR240 billion (US$3.01 billion) to set up a 6G AMOLED plant in Telangana State, central India, to produce smartphone, tablet and notebook applications.

India-based oil, gas and metal producer Vedanta has acquired Japan-based LCD glass substrate maker AvanStrate and applied to the India government for setting up a 8.6G TFT-LCD plant in India. Vedanta in February 2022 signed an MoU with Taiwan-based Foxconn Electronics to establish a joint-venture maker of semiconductors. As Taiwan-based LCD panel maker Innolux is AvanStrate"s client and has a 8.6G LCD plant in southern Taiwan, Vedanta could cooperate with Innolux via AvanStrate.

With subsidies under India government"s PLI scheme and UP Electronics Manufacturing Policy 2017 set by the state government of Uttar Pradesh, northern India, Samsung Display (SDC) invested US$654 million to set up a panel module factory in the state and started production in April 2021.

Samsung Electronics, SDC"s parent company, has cumulatively invested over US$1.1 billion in India and has been shifting production lines from China and Vietnam to India. The company has set up two large production bases and five R&D bases in India.

Although Samsung is expanding its production in India, clustering and production of its South Korea-based supply chain makers in India are currently much smaller than those in Vietnam.

China-based panel maker China Star Optoelectronics Technology (CSOT) has invested INR18.3 billion to set up a factory to produce 5- to 65-inch LCD modules in Andhra Pradseh, southeastern India. With annual production capacity of 8.0 million LCD modules, the factory is intended to mainly support TCL, CSOT"s parent company, to sell LCD TVs in the India market. TCL expects to sell 10 million LCD TVs for a market share of 7% in India in 2022. TCL currently ranks fourth in the India TV market and aims to surpass Sony, ranking third with a market share of 12% at present, by the end of 2022.

Taiwan-based LCD panel maker AU Optronics (AUO) has evaluated the feasibility of investing in India. There are problems concerning culture and government efficiency in India, AUO chairman Paul Peng has said.

Supply chains are indeed gradually shifting from concentrated production in a few places to distributed production in multiple locations, Peng indicated, adding that distributed production carries risks such as more complicated management for supply chains and increases in production cost.

There are many factors that need to be considered in setting up overseas factories, including ecosystem support, infrastructure and local talent, Peng said. India is not ideal in terms of these three factors, and exiting panel makers are quite unlikely to set up panel lines in India for the time being, Peng noted.

China-based panel makers had kept expanding production capacities for nearly 10 years and, as a result they together occupied over 60% of global production capacity for LCD panels as of 2021, followed by Taiwanese makers with 20%, South Korean ones with 10% and Japanese ones with 6%.

Since major Chinese makers are still expanding LCD panel production capacities, China"s combined share of global total will reach 70% in the mid- to long-term.

In view of diminishing competitiveness in LCD, SDC terminated LCD panel production in June 2022 and has shifted focus to AMOLED. Taiwanese LCD panel makers are expected to benefit from SDC"s exit but are still far less competitive against Chinese fellow makers in production capacity. Therefore, they have chosen not to expand production capacities and have focused on high value-added LCD panels.

It varies from different manufacturers who adopt different technology and work with different raw materials suppliers. In order to ensure the quality of tft lcd display module , it is necessary for a professional manufacturer to put necessary investment into raw materials selection before production. Except the well-selected material, the manufacture cost on it including especially high technology, labor investment, advanced equipment cost and so on is indispensable as well.

From basic design to execution, Shenzhen LCD Mall Limited continues to deliver quality display oled ahead of schedule at cost effective prices. Shenzhen LCD Mall is mainly engaged in the business of oled display and other product series. This product is known as bacterial resistance. During the fabric treating stage, antibacterial agent is permeated into the fabrics’ fiber to achieve the antibacterial effect. It is easy to install and maintain. Shenzhen LCD Mall exhibits its advantaged predominance in tft panel market. It comes with optionally GA, HDM, AV, BNC, DVI conversion/driver board.

The spirit of “customer-oriented” is the soul of our company’s development. We strive to meet customer requirements by virtue of production technology and technical level that are prior to the industry.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey