lcd panel market share manufacturer

The global LCD TV (Liquid Crystal Display Television) market was dominated by Samsung and remained so in 2021 with a market share of over 19 percent by sales volume. LG Electronics takes second place with close to 13 percent in the same year, to beat TLC, one of the well-established brands in this segment.Read moreMarket share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volumeCharacteristic202120202019----

TCL. (March 11, 2022). Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume [Graph]. In Statista. Retrieved December 20, 2022, from https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL. "Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume." Chart. March 11, 2022. Statista. Accessed December 20, 2022. https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL. (2022). Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume. Statista. Statista Inc.. Accessed: December 20, 2022. https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL. "Market Share of Leading Lcd Tv Manufacturers Worldwide from 2019 to 2021, by Sales Volume." Statista, Statista Inc., 11 Mar 2022, https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/

TCL, Market share of leading LCD TV manufacturers worldwide from 2019 to 2021, by sales volume Statista, https://www.statista.com/statistics/1266996/global-leading-manufacturers-lcd-tv-market-share-sales-volume/ (last visited December 20, 2022)

The upstream materials or components of the LCD panel industry mainly include liquid crystal materials, glass substrates, polarizing lenses, and backlight LEDs (or CCFL, which accounts for less than 5% of the market).

The middle reaches is the main panel factory processing and manufacturing, through the glass substrate TFT arrays and CF substrate, CF as upper and TFT self-built perfusion liquid crystal and the lower joint, and then put a polaroid, connection driver IC and control circuit board, and a backlight module assembling, eventually forming the whole piece of LCD module. The downstream is a variety of fields of application terminal-based brand, assembly manufacturers. At present, the United States, Japan, and Germany mainly focus on upstream raw materials, while South Korea, Taiwan, and the mainland mainly seek development in mid-stream panel manufacturing.

With the successive production of the high generation line in mainland China, the panel production capacity and technology level have been steadily improved, and the industrial competitiveness has been gradually enhanced. Nowadays, the panel industry is divided into three parts: South Korea, mainland China, and Taiwan, and mainland China is expected to become the no.1 in the world in 2019.

In the past decade, China’s panel display industryhas achieved leapfrog development, and the overall size of the industry has ranked among the top three in the world. Chinese mainland panel production capacity is expanding rapidly, although Japanese panel manufacturers master a large number of key technologies, gradually lose the price competitive advantage, compression panel production capacity. Panel production is concentrated in South Korea, Taiwan, and China, which is poised to become the world’s largest producer of LCD panels.

Up to 2016, BOE‘s global market share continued to increase: smartphone LCD, tablet PC display, and laptop display accounted for the world’s first market share, and display screen increased to the world’s second, while TV LCD remained the world’s third. In LCD TV panels, Chinese panel makers have accounted for 30 percent of global shipments to 77 million units, surpassing Taiwan’s 25.5 percent market share for the first time and ranking second only to South Korea.

In terms of the area of shipment, the area of board shipment of JD accounted for only 8.3% in 2015, which has been greatly increased to 13.6% in the first half of 2016, while the area of shipment of hu xing optoelectronics in the first half of 2015 was only 5.1%, which has reached 7.8% in the first half of 2016. The panel factories in mainland China are expanding their capacity at an average rate of double-digit growth and transforming it into actual shipments and areas of shipment. On the other hand, although the market share of South Korea, Japan, and Taiwan is gradually decreasing, some South Korean and Japanese manufacturers have been inclined to the large-size HD panel and AMOLED market, and the production capacity of the high-end LCD panel is further concentrated in mainland China.

Domestic LCD panel production line capacity gradually released, overlay the decline in global economic growth, lead to panel makers from 15 in the second half began, in a low profit or loss, especially small and medium-sized production line, the South Korean manufacturers take the lead in transformation strategy, closed in medium and small size panel production line, South Korea’s 19-panel production line has shut down nine, and part of the production line is to research and development purposes. Some production lines are converted to LTPS production lines through process conversion. Korean manufacturers are turning to OLED panels in a comprehensive way, while Japanese manufacturers are basically giving up the LCD panel manufacturing business and turning to the core equipment and materials side. In addition to the technical direction of the research and judgment, more is the LCD panel business orders and profits have been severely compressed, Korean and Japanese manufacturers have no desire to fight. Since many OLED technologies are still in their infancy in mainland China, it is a priority to move to high-end panels such as OLED as soon as possible. Taiwanese manufacturers have not shut down factories on a large scale, but their advantages in LCD technology and OLED technology have been slowly eroded by the mainland.

STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.

The global TFT-LCD display panel market attained a value of USD 181.67 billion in 2022. It is expected to grow further in the forecast period of 2023-2028 with a CAGR of 5.2% and is projected to reach a value of USD 246.25 billion by 2028.

The current global TFT-LCD display panel market is driven by the increasing demand for flat panel TVs, good quality smartphones, tablets, and vehicle monitoring systems along with the growing gaming industry. The global display market is dominated by the flat panel display with TFT-LCD display panel being the most popular flat panel type and is being driven by strong demand from emerging economies, especially those in Asia Pacific like India, China, Korea, and Taiwan, among others. The rising demand for consumer electronics like LCD TVs, PCs, laptops, SLR cameras, navigation equipment and others have been aiding the growth of the industry.

TFT-LCD display panel is a type of liquid crystal display where each pixel is attached to a thin film transistor. Since the early 2000s, all LCD computer screens are TFT as they have a better response time and improved colour quality. With favourable properties like being light weight, slim, high in resolution and low in power consumption, they are in high demand in almost all sectors where displays are needed. Even with their larger dimensions, TFT-LCD display panel are more feasible as they can be viewed from a wider angle, are not susceptible to reflection and are lighter weight than traditional CRT TVs.

The global TFT-LCD display panel market is being driven by the growing household demand for average and large-sized flat panel TVs as well as a growing demand for slim, high-resolution smart phones with large screens. The rising demand for portable and small-sized tablets in the educational and commercial sectors has also been aiding the TFT-LCD display panel market growth. Increasing demand for automotive displays, a growing gaming industry and the emerging popularity of 3D cinema, are all major drivers for the market. Despite the concerns about an over-supply in the market, the shipments of large TFT-LCD display panel again rose in 2020.

North America is the largest market for TFT-LCD display panel, with over one-third of the global share. It is followed closely by the Asia-Pacific region, where countries like India, China, Korea, and Taiwan are significant emerging market for TFT-LCD display panels. China and India are among the fastest growing markets in the region. The growth of the demand in these regions have been assisted by the growth in their economy, a rise in disposable incomes and an increasing demand for consumer electronics.

The report gives a detailed analysis of the following key players in the global TFT-LCD display panel Market, covering their competitive landscape, capacity, and latest developments like mergers, acquisitions, and investments, expansions of capacity, and plant turnarounds:

*At Expert Market Research, we strive to always give you current and accurate information. The numbers depicted in the description are indicative and may differ from the actual numbers in the final EMR report.

Westford,USA, Oct. 19, 2022 (GLOBE NEWSWIRE) -- The primary factors driving the growth of the Display Market are increasing demand from smartphone and tablet manufacturers, rising expenditure on smart Infra-Red (IR) sensors, and rapid expansion of digital media content. Smartphones are becoming more sophisticated and are using larger screens that require higher resolutions for better user experience. Tablets are also becoming increasingly popular as they offer a single device that can serve as both a computer and a mobile phone. This increase in demand for high-resolution displays is expected to drive the adoption of LED displays in the coming years.

Manufacturers in the global display market are starting to see the potential in displays as an important part of their product lines. Device manufacturers are looking for displays that can be used on a variety of devices, from laptops to smartphones and even cars. In addition, developers are creating more applications that require high-quality displays.

One key challenge facing manufacturers is making sure that their displays meet the requirements of multiple market segments. They need to make sure that their displays are suitable for usage on tablets as well as laptops, yet they also need to create displays that look good on smaller devices like smartphones and digital assistants.

The growth in demand for display market across various verticals such as healthcare, retail, automotive, appliance and others has led to an increasing demand for large sizes screens which can be cost effective owing to their mass production capabilities. Display manufacturers are also exploring new technologies such as flexible displays that can be rolled up like a traditional newspaper

Our report considers several factors such as market size estimation techniques, product segmentation analysis, expenditure Breakdown by Country and region; Porter"s Five Forces Analysis; and price trends analysis to give you a comprehensive view of the global display market.

Some of the key players in the global display market include LG Display Co., Ltd., Samsung Electronics Co., Ltd., and Sharp Corporation. These companies are focused on developing innovative products that meet the needs of various consumers in the marketplace. They also strive to improve their competitiveness by expanding their product lines into new markets and by creating partnerships with other companies to share technology and manufacturing resources.

Among global display market leaders, Samsung is presently dominating the industry with a share of 38% of the market. However, Apple is looming large as one of the largest competitors in smartphone sector. Other prominent players in this segment include LG Display, Sony Corp, and Toshiba Corporation. Among these companies, LG Display has been fastest expanding its business over recent years owing to its focus on emerging markets such as China and India.

For one, it"s heavily invested in research and development in the display market. According to analysts at SkyQuest, Samsung spends more than $13.7 billion a year on R&D, more than any other company in the world. That investment has paid off: The company"s displays are consistently among the best on the market.

Samsung also makes good use of its deep pockets. The company has poured money into forming joint ventures with major chipmakers like Qualcomm and Intel, which allows it to quickly bring new technologies to market. It doesn"t just rely on partnerships; Samsung also invests in its own technology centers, such as the foundry that produces screens for its smartphones.

One important technology that Samsung is investing in is AMOLED and QLED screens. QLEDs are generally considered to be more environmentally friendly than LCDs, since they use less power and create fewer byproducts.

The main drivers for Samsung"s strong performance in the display market are its diversification across product lines, continuous innovation across product categories, and excellent execution capabilities. The company has been able to expand into new markets such as automotive displays and smart watches, while continuing to focus on profitable core products.

Samsung has also been successful in pushing down prices for OLED displays over the past few years. This has made OLED panels more accessible to a wider range of customers, supporting growth at rival companies such as LG Electronics and Sony.

In recent years, there has been a shift in display technology as manufacturers across the global display market experiment with new and more innovative ways to create displays. The trend observed by SkyQuest worldwide is that display technologies are moving towards OLEDs and quantum dots, both of which have a number of advantages.

Quantum dots or QLED offer many advantages over traditional LCDs in the display market, such as better color reproduction, enhanced viewing angles, better response time, and lower power consumption. Their small size also makes them ideal for applications where sliding or tilting LCD panels are not possible or desirable. Quantum dot displays have already begun appearing in consumer electronics and will eventually replace traditional LCDs as the predominant type of display in devices like smartphones and tablets.

SkyQuest Technology is leading growth consulting firm providing market intelligence, commercialization and technology services. It has 450+ happy clients globally.

According to IMARC Group’s latest report, titled “TFT LCD Panel Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2022-2027”, the global TFT LCD panel market size reached US$ 157 Billion in 2021. Looking forward, IMARC Group expects the market to reach US$ 207.6 Billion by 2027, exhibiting a growth rate (CAGR) of 4.7% during 2022-2027.

A thin-film-transistor liquid-crystal display (TFT LCD) panel is a liquid crystal display that is generally attached to a thin film transistor. It is an energy-efficient product variant that offers a superior quality viewing experience without straining the eye. Additionally, it is lightweight, less prone to reflection and provides a wider viewing angle and sharp images. Consequently, it is generally utilized in the manufacturing of numerous electronic and handheld devices. Some of the commonly available TFT LCD panels in the market include twisted nematic, in-plane switching, advanced fringe field switching, patterned vertical alignment and an advanced super view.

We are regularly tracking the direct effect of COVID-19 on the market, along with the indirect influence of associated industries. These observations will be integrated into the report.

The global market is primarily driven by continual technological advancements in the display technology. This is supported by the introduction of plasma enhanced chemical vapor deposition (PECVD) technology to manufacture TFT panels that offers uniform thickness and cracking resistance to the product. Along with this, the widespread adoption of the TFT LCD panels in the production of automobiles dashboards that provide high resolution and reliability to the driver is gaining prominence across the globe. Furthermore, the increasing demand for compact-sized display panels and 4K television variants are contributing to the market growth. Moreover, the rising penetration of electronic devices, such as smartphones, tablets and laptops among the masses, is creating a positive outlook for the market. Other factors, including inflating disposable incomes of the masses, changing lifestyle patterns, and increasing investments in research and development (R&D) activities, are further projected to drive the market growth.

The competitive landscape of the TFT LCD panel market has been studied in the report with the detailed profiles of the key players operating in the market.

IMARC Group is a leading market research company that offers management strategy and market research worldwide. We partner with clients in all sectors and regions to identify their highest-value opportunities, address their most critical challenges, and transform their businesses.

IMARC’s information products include major market, scientific, economic and technological developments for business leaders in pharmaceutical, industrial, and high technology organizations. Market forecasts and industry analysis for biotechnology, advanced materials, pharmaceuticals, food and beverage, travel and tourism, nanotechnology and novel processing methods are at the top of the company’s expertise.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

The Liquid Crystal Display (LCD)-enabled electronic devices, such as television, mobile phones and others, is creating potential opportunities for the LCD panel market. In the past couple of years, LCD panels have gained popularity owing to their advanced properties that include less power consumption, compact size and low price.

Moreover, over the past two decades, the LCD technology of has made impressive progress. The electronic displays available at present make use of a wide variety of active LCD panels. The LCD panel market is one of the significantly growing markets due to the increasing demand for LCD displays & low power consumption electronic goods, as well as increase in the demand for touch-enabled displays.

An LCD panel is designed to project on-screen information. At present, LCD panels are suited with high-mobility electronic equipment. LCDs with improved video quality are gaining momentum in all developed and developing economies. These factors are projected to propel the global LCD panel market.

The major growth drivers of the LCD panel market include an increase in the demand for energy-efficient electronic products as well as for larger and 4K televisions. Furthermore, growth in the demand for energy-efficient electronic devices is surging the global LCD panel market.

Demand for high-quality screens, coupled with improving standards of living and inflating disposable income, are among key factors boosting the LCD Panel market. In addition, increase in the adoption of consumer electronic devices is projected to drive the global LCD panel market.

However, one of the major challenges of the LCD panel market are the higher cost and thickness of the display of these devices as compared to other modules. The LCD panel market is expected to witness sluggish and unpredictable growth owing to a quantitative decline in the number of LCD displays.

Moreover, financial uncertainty and macroeconomic situations around the world, such as fluctuating currency exchange rates and economic difficulties, are some of the major factors hindering the growth of the LCD panel market. However, increased competition from alternative technologies and LCD panel complex structure is likely to limit the growth of the LCD panel market.

At present, North America holds the largest market share for the LCD panel market due an increase in the demand for consumer electronic devices. Due to the presence of key LCD panel manufacturers in China and Japan, Asia Pacific is expected to become the prominent region for the LCD panel market.

In addition, the unorganized market of LCD panels in China, Japan and India is creating a competitive environment for global LCD panel manufacturers. Moreover, Europe is the fastest-growing market for LCD panels due to an increase in the adoption of consumer electronics devices. The demand for LCD panels has risen dramatically over the past 12 months globally. The usage of LCD displays in various industries in these regions is boosting the LCD panel market.

The report is a compilation of first-hand information, qualitative and quantitative assessment by industry analysts, inputs from industry experts and industry participants across the value chain. The report provides in-depth analysis of parent market trends, macro-economic indicators and governing factors along with market attractiveness as per segments. The report also maps the qualitative impact of various market factors on market segments and geographies.

Due to an increase in the demand for large LCD displays, the large size LCD panel sub-segment is expected to register double-digit growth rate in the global market. In addition, due to an increase in the demand for portable electronic devices, the small size LCD panel sub-segment is projected to be the most attractive market sub-segment of the global LCD panel market.

The smart phones and tablets sub-segment held the largest market share for the LDC panel market in 2017, and the wearable devices sub-segment is expected to grow with a high CAGR during the forecast period.

The global display market size was valued at $114.9 billion in 2021, and is projected to reach $216.3 billion by 2031, growing at a CAGR of 6.7% from 2022 to 2031.

Display includes screen, computer output surface, and a projection surface that displays content, mainly test, graphics, pictures, and videos utilizing cathode ray tube (CRT), light-emitting diode (LED), liquid crystal display (LCD), and other technologies. These displays are majorly incorporated in devices such as televisions, smartphones, tablets, laptops, vehicles, and others. Emergence of advanced technologies offer enhanced visualizations in several industry verticals, which include consumer electronics, retail, sports & entertainment, and transportation. 3D displays are in trend in consumer electronics and entertainment sector.

In addition, flexible display technologies witness popularity at a high pace. Moreover, display technologies such as organic light-emitting diode (OLED) have gained increased importance in products such as televisions, smart wearables, smartphones, and other devices. Smartphone manufacturers plan to incorporate flexible OLED displays to attract consumers. Furthermore, the market is also in the process of producing energy saving devices, primarily in wearable devices. However, high cost of the transparent and quantum dot display technologies. Hence, need for such high costs associated with display products may hamper growth of the market. Furthermore, adoption of AR/VR devices and commercialization of autonomous vehicles are expected to provide lucrative display market opportunity for the growth of the market.

The COVID-19 pandemic is impacting the society and overall economy across the global. The impact of this outbreak is growing day-by-day as well as affecting the supply chain. It is creating uncertainty in the massive slowing of supply chain, and increasing panic among customers. European countries under lockdowns have suffered major loss of business and revenue due to shutdown of manufacturing units in the region. Operations of production and manufacturing industries have been heavily impacted by the outbreak of COVID-19, which led to slowdown in the display market growth.

By display type, the display market outlook is divided into flat panel display, flexible panel display, and transparent panel display. Flat panel display segment was the highest revenue contributor to the market, in 2021. The flexible panel display segment dominated the display market growth, in terms of revenue, in 2021, and is expected to follow the same trend during the forecast period.

By industry vertical, the market it is divided into healthcare, consumer electronics, retail, BFSI, military & defense, transportation, and others.Consumer electronics accounted for largest display market share in 2021.

Region wise, the display market trends are analyzed across North America (the U.S., Canada, and Mexico), Europe (UK, Germany, France, and rest of Europe), Asia-Pacific China, Japan, India, South Korea, and rest of Asia-Pacific), and LAMEA (Latin America, the Middle East, and Africa). Asia-Pacific, specifically the China, remains a significant participant in the global display industry. Major organizations and government institutions in the country are intensely putting resources into these displays.

Top impacting factors of the market include high demand for flexible display technology in consumer electronic devices, increase in adoption of electronic components in the automotive sector, and rise in trend of touch-based devices. Surge in adoption of displays in touch screen devices, rise in need for AR/VR devices, and commercialization of autonomous vehicles are expected to create lucrative in the future. Moreover, stagnant growth of desktop PCs, notebooks, and tablets hampers growth of the display market. However, each of these factors is expected to have a definite impact on growth of the display industry in the coming years.

The key players profiled in this report include LG Display Co. Ltd., Samsung Electronics Co. Ltd., AU Optronics, Japan Display Inc., E Ink Holdings Inc., Hannstar Display Corporation, Corning Incorporated, Kent Displays Inc., NEC Display Solutions, and Sony Corporation. These key players have adopted strategies, such as product portfolio expansion, mergers & acquisitions, agreements, regional expansion, and collaborations to enhance their market penetration.

KEY BENEFITSFOR STAKEHOLDERSThis study comprises analytical depiction of the display market forecast along with the current trends and future estimations to depict the imminent investment pockets.

Key Market Players Samsung Electronics Co Ltd, Sharp Corporation, Japan Display Inc, Innolux Corporation, NEC CORPORATION, Panasonic Corporation, BOE Technology Group Co., Ltd., AUO Corporation, Sony Corporation, Leyard Optoelectronic Co., Ltd, LG Display Co Ltd

Display panel is a component that displays information in form of text, picture, video, and others. It acts as a direct interface in human and machine interaction. Display panels are used in variety of equipments, such as TV, smartphone, tablets, PCs, and others. Innovations in display technologies are focused on reducing harmful effects on health of end user. The technological advancements in display panel enhance viewing experience, consume less electricity, and dissipate less heat.

Growing demand for large-sized OLED panels for television and demand for public & commercial display panels drive growth of the world display panel market. However, decrease in ASP and revenues due to overcapacity obstruct growth of the market. On the other hand, demand for flexible displays for mobile phones and increasing focus on R&D activities open up new opportunities in the market.

The world display panel market is segmented based on technology, size, farm factor, resolution, applications, and geography. The technology segment is further classified into LED, OLED, and others. On the basis of size, the market is divided into small, medium, and large. Flat and flexible are farm factors discussed in the report. On the basis of resolution, the market is classified into 8K, 4K, WQHD, FHD, HD, and others. Applications covered in the report are TV, desktop monitor, notebook PC, tablet, mobile phone, automotive, digital signage, and others. Geographically, the market is divided into North America, Asia-Pacific, Europe, and Latin America, Middle East and Africa (LAMEA).

The prominent companies operating in the market are LG Display Co. Ltd., Samsung Electronics Co. Ltd., Innolux Corporation, AU Optronics Corp., Sharp Corporation, Japan Display Inc., BOE Technology Group Co. Ltd., Panasonic Corporation, HannStar Display Corporation, and Chunghwa Picture Tubes Ltd. The key strategies adopted by these manufacturers to strengthen their position in the market are collaborations, approvals, mergers & acquisitions, partnerships, joint ventures, expansions, and others.

This report offers an in-depth quantitative analysis of the current market and estimations through 2015-2020, which assists in identifying the prevailing market opportunities.

An extensive analysis of current research and clinical developments withinthe world display panel market is provided with key market dynamic factors that help in understanding the behavior of the market.

Key Market Players Sony Corporation, Panasonic Corporation, Toshiba Corporation, LG Display Co. Ltd, Samsung Electronics Co. Ltd, Japan Display, Leyard Optoelectronic, AU Optronics, BOE Technology, NEC Corporation

Flat-panel displays are thin panels of glass or plastic used for electronically displaying text, images, or video. Liquid crystal displays (LCD), OLED (organic light emitting diode) and microLED displays are not quite the same; since LCD uses a liquid crystal that reacts to an electric current blocking light or allowing it to pass through the panel, whereas OLED/microLED displays consist of electroluminescent organic/inorganic materials that generate light when a current is passed through the material. LCD, OLED and microLED displays are driven using LTPS, IGZO, LTPO, and A-Si TFT transistor technologies as their backplane using ITO to supply current to the transistors and in turn to the liquid crystal or electroluminescent material. Segment and passive OLED and LCD displays do not use a backplane but use indium tin oxide (ITO), a transparent conductive material, to pass current to the electroluminescent material or liquid crystal. In LCDs, there is an even layer of liquid crystal throughout the panel whereas an OLED display has the electroluminescent material only where it is meant to light up. OLEDs, LCDs and microLEDs can be made flexible and transparent, but LCDs require a backlight because they cannot emit light on their own like OLEDs and microLEDs.

Liquid-crystal display (or LCD) is a thin, flat panel used for electronically displaying information such as text, images, and moving pictures. They are usually made of glass but they can also be made out of plastic. Some manufacturers make transparent LCD panels and special sequential color segment LCDs that have higher than usual refresh rates and an RGB backlight. The backlight is synchronized with the display so that the colors will show up as needed. The list of LCD manufacturers:

Organic light emitting diode (or OLED displays) is a thin, flat panel made of glass or plastic used for electronically displaying information such as text, images, and moving pictures. OLED panels can also take the shape of a light panel, where red, green and blue light emitting materials are stacked to create a white light panel. OLED displays can also be made transparent and/or flexible and these transparent panels are available on the market and are widely used in smartphones with under-display optical fingerprint sensors. LCD and OLED displays are available in different shapes, the most prominent of which is a circular display, which is used in smartwatches. The list of OLED display manufacturers:

MicroLED displays is an emerging flat-panel display technology consisting of arrays of microscopic LEDs forming the individual pixel elements. Like OLED, microLED offers infinite contrast ratio, but unlike OLED, microLED is immune to screen burn-in, and consumes less power while having higher light output, as it uses LEDs instead of organic electroluminescent materials, The list of MicroLED display manufacturers:

LCDs are made in a glass substrate. For OLED, the substrate can also be plastic. The size of the substrates are specified in generations, with each generation using a larger substrate. For example, a 4th generation substrate is larger in size than a 3rd generation substrate. A larger substrate allows for more panels to be cut from a single substrate, or for larger panels to be made, akin to increasing wafer sizes in the semiconductor industry.

"Samsung Display has halted local Gen-8 LCD lines: sources". THE ELEC, Korea Electronics Industry Media. August 16, 2019. Archived from the original on April 3, 2020. Retrieved December 18, 2019.

"TCL to Build World"s Largest Gen 11 LCD Panel Factory". www.businesswire.com. May 19, 2016. Archived from the original on April 2, 2018. Retrieved April 1, 2018.

"Panel Manufacturers Start to Operate Their New 8th Generation LCD Lines". 대한민국 IT포털의 중심! 이티뉴스. June 19, 2017. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"TCL"s Panel Manufacturer CSOT Commences Production of High Generation Panel Modules". www.businesswire.com. June 14, 2018. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"Samsung Display Considering Halting Some LCD Production Lines". 비즈니스코리아 - BusinessKorea. August 16, 2019. Archived from the original on April 5, 2020. Retrieved December 19, 2019.

Herald, The Korea (July 6, 2016). "Samsung Display accelerates transition from LCD to OLED". www.koreaherald.com. Archived from the original on April 1, 2018. Retrieved April 1, 2018.

"China"s BOE to have world"s largest TFT-LCD+AMOLED capacity in 2019". ihsmarkit.com. 2017-03-22. Archived from the original on 2019-08-16. Retrieved 2019-08-17.

A flat panel display (FPD) is an electronic view device that allows people to see content such as text or moving images in different consumer electronics, mobile devices, and a range of entertainment. FPDs are thinner and lighter than conventional cathode ray tubes (CRT), which is usually less than 10 centimeters. There are two different categories of FPDs namely emissive displays and non-emissive displays. LED is an example of an emissive display, while LCD is an example of non-emissive display. These displays are majorly used in TV monitors, laptop computers, portable electronics, digital cameras, packet video games, etc. FPDs offer high pixel resolution, enhanced contrast setting, and lower power consumption.

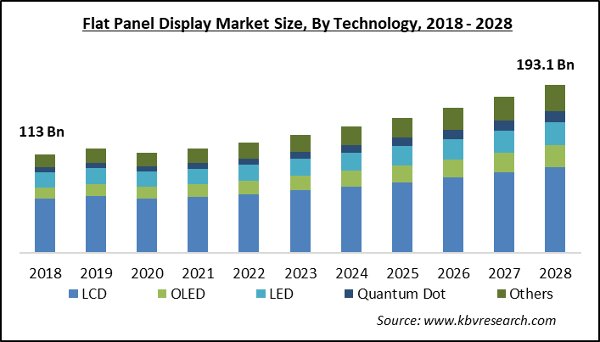

The global flat panel display market is estimated to be valued at US$ 142,155 million in 2021 and is expected to exhibit a CAGR of 5.8 % over the forecast period (2021-2028).

In August 2019, LG Display announced the opening of its 8.5th generation (2,200mm x 2,500mm) OLED panel production plant in Guangzhou, China, to produce 10 million large-size OLED panels a year.

Asia Pacific excluding Japan held dominant position in the global mobile phone accessories market in 2020, accounting for 84.8% share in terms of Value, followed by Europe and Americas, respectively.

Rising government support to FPD industry is expected to drive growth of the global flat panel display market during the forecast period. Rising government initiatives and proactive support have led to rapid development of flat panel industry in major economies including Japan, Canada, and the U.S. For instance, the government of Japan has shown keen interest in the development of high-resolution screens. On the contrary, the U.S. Government is supporting FPD industry, which is primarily channeled through the Department of Defense. Moreover, the Korean government provides support for development of the high tech industry.

Growing adoption of FPD in mobile devices is expected to propel the global flat panel display market growth over the forecast period. Increasing demand for smartphones with augmented features is a major driving factor in the market. Smartphone manufacturers are focused on adopting FPD technology, in order to cater to increasing demand for high-quality image and clarity. FPD offers enhanced picture quality with improved contrast setting and low power consumption.

FPDs are being increasingly deployed in various application areas, especially in retail segment. Major demand for LCD and PDP technologies is arising from the retail segment for application in flat digital signage Majority of small flat panel digital signage installations are taking place in retail stores and Quick Service Restaurants (QSRs).

LCD manufacturers are innovating their LCD product line and introducing new technology to sustain in the LCD panel market. For instance, in 2012, Samsung commercialized production of a transparent LCD panel for a wide variety of display applications such as platform doors of subways, commercial freezer doors, e-Boards, medical equipment, and mobile devices.

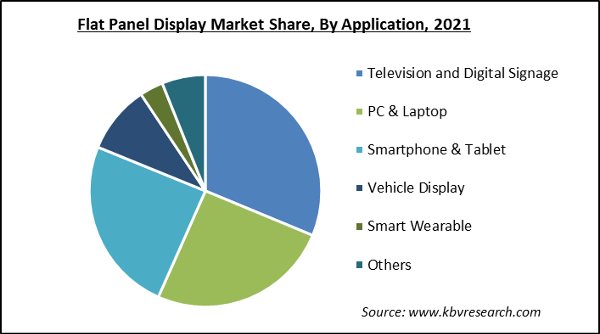

By Application: Consumer Electronics (LCD Television (TV), Mobile Phone, Personal Computer (PC)), Automotive Application, Others (Healthcare, Defense, Military, Aviation, Automotive)

Development in glass OLED panels has led to next-generation displays such as plastic OLED panels. These OLED panels utilize plastic substrate instead of a conventional glass substrate that has various applications. For instance, in 2013, LG Display introduced the world’s first display manufacturer to provide mass-produced flexible OLED panels for smartphones. It is expected to expand further into diverse applications including automobile displays, tablets, etc.

The liquid crystal display (LCD) segment held dominant position in the market and accounted for 38% share in the global flat panel display market in 2020. The segment is expected to reach US$ 124,042.18 million in 2028. This is owing to the wider angles and large display area offered by LCD.

The consumer electronics segment held a dominant position and accounted for 87% share in the global flat panel display market in 2020. This is segment is expected to be valued US$ 99,939.82 million by 2028, owing to growing demand for television and smartphones.

Saturation in the market is expected to restrain growth of the global flat panel display market during the forecast period. Popularity of LCDs is high due to engagement of some of the top players such as Samsung, LG, Panasonic, etc. However, the trend is rapidly changing, owing to the introduction of more powerful technologies such as OLED, which is gaining popularity among major players in the market. Key companies in the market such as Apple are shifting towards OLED displays for application in its products such as iPad, iPhone, iTV, iWatch, etc.

Restricted view angle of LCD is expected to hinder the global flat panel display market growth over the forecast period. LCD technologies have a major drawback, restricted viewing angle. As a result of this, images and brightness on a television screen do not appear in true color when viewed from every angle. Several technologies have been developed to address this issue; however, OLED televisions seem to be the best option in this regard.

Key companies involved in the global flat panel display market are Sony Corporation, AU Optronics Corp., Panasonic Corporation, Emerging Display Technologies Corp., LG Display Co. Ltd., Innolux Corp., Universal Display Corporation, Japan Display Inc., and Samsung Electronics Co. Ltd.

Major companies in the market are focused on product launches, in order to expand product portfolio. For instance, in January 2020, Sony Corporation launched Bravia displays and a crystal LED display at ISE 2020.

Key players in the market are involved in partnerships and collaborations, in order to gain a competitive edge in the market. For instance, August 2019, Universal Display Corporation partnered with Eternal Material Technology Company to commercialize OLED host materials.

Display Market size was valued at USD 127.2 Billion in 2020 and is projected to reach USD 160.36 Billion by 2028, growing at a CAGR of 2.9% from 2021 to 2028.

The major factors driving industry growth are the increasing adoption of OLED displays in smartphones huge investments, coupled with government support for the construction of new OLED and LCD panel manufacturing facilities are the major factors expected to propel the Display Market. Increasing demand for 4K and 8K displays with the availability of UHD content and increasing deployment of HUD, central stack display, and instrument cluster in automotive vehicles are some other factors that support market growth. Moreover, the emerging use cases such as smart displays, smart mirrors, smart home appliances, and holographic displays can create the opportunity for market growth.

A screen, a computer output surface, and a projection surface display text and graphics using a cathode ray tube, light-emitting diode, liquid crystal display, or other technologies. It may be used in a variety of areas, including television, cellphones, tablets, laptops, cars, public transportation, and many others. The growing demand for OLED-based products, technological advancements and the development of smart wearable devices, and expansion in the flexible device industry are all key market drivers. However, as smart mirrors and smart displays become more widely used in many end-use sectors, firms in the target market may see increased income prospects.

The usage of organic light-emitting diode screens in smartphones and televisions is driving the Display Market forward. Another element driving target market expansion is the use of technologically superior, lightweight, thin, and energy-efficient displays. Furthermore, the growing popularity of smart wearables among consumers is projected to fuel the Display Market growth in the near future. However, the Global Display Market growth is being hampered by changing display panel costs and the high cost of technologically sophisticated display panels.

The major factors driving industry growth are the increasing adoption of OLED displays in smartphones; huge investments, and coupled government support for the construction of new OLED and LCD panel manufacturing facilities, and these are the major factors expected to propel the targeted market. Increasing demand for 4K and 8K displays with the availability of UHD content and increasing deployment of HUD, central stack display, and instrument cluster in automotive vehicles are some other factors that support market growth.

The deployment of wide-screen alternatives, such as projectors and screen-less displays might act as hindering factor. Moreover, the emerging use cases such as smart displays, smart mirrors, smart home appliances, and holographic displays can create the opportunity for market growth. Nowadays, display gadgets are also used in the car business. LG Display, for example, has declared that it will begin production of a head-up display system for the vehicle industry in response to this potential. LG’s vehicle display gadget is a flexible, transparent display that can be wheeled about. The heads-up display may be used in a variety of ways and has a variety of functions to improve your driving experience.

As touch-based gadgets have become more accessible in recent years, the number of devices using touch sensors has expanded tremendously. Touch-based devices necessitate the use of a display panel, which aids in the growth of display devices. As a result, a large range of home appliances, such as refrigerators, microwaves, washing machines, chimneys, and others, are equipped with touch-sensitive displays. Furthermore, the automobile industry has seen an increase in the use of advanced display devices in vehicles, such as navigation systems, digital dashboards, digital rearview mirrors, and heads-up displays, among others.

Due to the complicated and enormous architecture of commercial buildings such as malls, theatres, entertainment centers, and others, the use of digital signage and touch-based displays has expanded. Touch sensors are built into these screens, which the user can use to navigate and extract other information. As a result, the expansion of the Display Market is fueled by the trend of touch-based gadgets.

Based on Display Type, The market is segmented into Flat Panel Display, Transparent Panel Display, Flexible & Foldable Panel Display, And 3D Display. The Global Display Market is being driven by advancements in flexible displays, an increase in demand for OLED display devices, and a rise in the popularity of touch-based devices. However, the market is hampered by the high cost of new display technologies such as transparent displays and quantum dot screens, as well as the sluggish growth of desktop PCs, notebooks, and tablets. Furthermore, the Global Display Market is likely to benefit from new applications in flexible display technologies, which are expected to generate lucrative growth prospects.

Based on Technology, The market is segmented into OLED, LED, Micro-LED, Direct-View LED, LCD, And Others. Over the previous few decades, LCD technology has been widely used in display products. LCD-based devices are currently used in a variety of areas, including retail, corporate offices, and banks. During the forecast period, however, LED technology is expected to grow at a rapid pace. The market for LED technology is being driven by advancements in LED technology and its energy-efficient nature. High competition from newer technologies, a disruption in the supply-demand ratio, and a drop in LCD display panel ASPs are likely to force the LCD display industry into negative growth throughout the projection period.

Based on Product, The market is segmented into Smartphone, Television, PC Monitor & Laptop, Automotive Display, And Others. Smartphones are likely to account for a significant portion of the industry. The rising usage of OLED and flexible screens by smartphone makers will drive this growth. Shipments of high-cost flexible OLED displays are rapidly expanding, and this trend is projected to continue during the forecast period. The smart wearables segment has emerged as the global market’s new growth route. The market for these devices is fast-growing, and with the widespread adoption of AR/VR technologies, demand for smart wearables is likely to skyrocket over the forecast period.

Based on Industry, The market is segmented into Consumer, Transportation, Retail, Hospitality & BFSI, Education, Healthcare, Military, Defense, and Aerospace, And Others.

Based on Geography, The Global Display Market is classified into North America, Europe, Asia Pacific, and the Rest of the world. The Display Market is dominated by North America, which is predicted to develop at a healthy rate in terms of earnings over the projection period. Because of their high disposable income, consumers are adopting technologically improved electronic products, which is driving market expansion. In the foreseeable future, the market is projected to see significant earnings growth. The target market in the region is driven by the existence of core performance manufacturing.

The “Global Display Market” study report will provide valuable insight with an emphasis on the global market. The major players in the market are LG Display, AU Optronics, Japan Display (JDI), Tianma Microelectronics, Samsung Electronics, SHARP (Foxconn), Truly International, BOE Technology, Innolux Corporation, and China Star Optoelectronics Technology (CSOT) (CDOT) (TCL).

Our market analysis also entails a section solely dedicated to such major players wherein our analysts provide an insight into the financial statements of all the major players, along with its product benchmarking and SWOT analysis. The competitive landscape section also includes key development strategies, market share, and market ranking analysis of the above-mentioned players globally.

In January 2019, the first 15.6-inch OLED panel has been introduced by Samsung Electronics in the notebook market. In addition, the panel will deliver brighter colors and deeper blacks compared to 4K LCD-based screens.

To know more about the Research Methodology and other aspects of the research study, kindly get in touch with our Sales Team at Verified Market Research.

• Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

• Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

• The current as well as the future market outlook of the industry with respect to recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

Display Market was valued at USD 127.2 Billion in 2020 and is projected to reach USD 160.36 Billion by 2028, growing at a CAGR of 2.9% from 2021 to 2028.

Increasing demand for 4K and 8K displays with the availability of UHD content and increasing deployment of HUD, central stack display, and instrument cluster in automotive vehicles are some other factors that support market growth.

The sample report for the Display Market can be obtained on demand from the website. Also, the 24*7 chat support & direct call services are provided to procure the sample report.

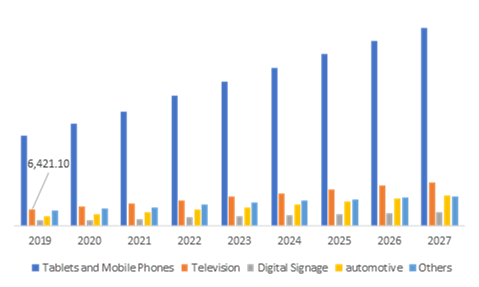

This market research report includes a detailed segmentation of the global large area LCD display market by application (TVs, notebooks, monitors, tablets, and others). It outlines the market shares for key regions such as the Americas, APAC, and EMEA. The key vendors analyzed in this report are AU Optronics, BOE Technology, Innolux, LG Display, and Samsung Display.

Technavio’s research analyst predicts the global large area LCD display market to grow at a CAGR of 3% during the forecast period. The formation of UHD alliances is the primary growth driver for this market. During 2015, supply chain members of the global UHD TV market announced the formation of the UHD Alliance to support innovative technologies including 4K and higher resolution, high dynamic range, immersive 3D audio, and wider color gamut.

The decline in ASP of the LCD panel is expected to boost the market growth during the forecast period. During 2014, per meter square, ASP of LCD panel was $472, which declined to $416 during 2015. Vendors reduced the ASP to reduce excess inventory. The declining per square meter ASP of LCD panel drove the shipment of LCD display in terms of area.

During 2015, the TV segment dominated the large area LCD display market with a market share of 38%. The primary reason for the growth of this product segment was the strong demand for 4K TVs of 40 inches and larger screen size. During 2015, several manufacturers introduced 4K TVs ranging from 50 inches and above.

During 2015, APAC accounted for 81% of the market share and is expected to grow at a CAGR of 1% during the forecast period. The high concentration of display device manufacturers and LCD panel manufacturers in this region are the primary growth drivers. Technavio expects that the well-established supply chain for display devices in APAC would continue to support the dominance of this region in the market during the forecast period. China is emerging fast as a leading hub for large area TFT LCD display manufacturers because of the rise in the number of display device manufacturers in the country.

Manufacturing LCD display panels require economies of scale because the equipment used to manufacture displays are expensive. This presents high entry barriers for LCD display panel manufacturers. Currently, the global large area LCD display market is dominated by China, Japan, South Korea, and Taiwan in terms of production and revenue contribution. Chinese manufacturers have the advantage of manufacturing LCD panels at a lower cost. This has resulted in price wars among LCD manufacturers and has accelerated the declining ASP of LCD panels. Vendors such as LG and Samsung are under a lot of pressure as profit margins have come down because of increased competition.

Other prominent vendors in the market include Chi Mei Optoelectronics, Chunghwa Picture Tube (CPT), HannsTouch Solution, HannStar Display, InfoVision Optoelectronics, Japan Display, Kaohsiung Opto-Electronics, NEC Display Solutions, Panasonic, and Sharp.

LCD TV Panel Market is 2022 Research Report on Global professional and comprehensive report on the LCD TV Panel Market. The report monitors the key trends and market drivers in the current scenario and offers on the ground insights. Top Key Players are – Samsung Display, LG Display, Innolux Crop., AUO, CSOT, BOE, Sharp, Panasonic, CEC-Panda.

Global “LCD TV Panel Market” (2022-2028) the report additionally centers around worldwide significant makers of the LCD TV Panel market with important data, such as, company profiles, segmentation information, challenges and limitations, driving factors, value, cost, income and contact data. Upstream primitive materials and hardware, coupled with downstream request examination is likewise completed. The Global LCD TV Panel market improvement patterns and marketing channels are breaking down. In conclusion, the attainability of new speculation ventures is surveyed and in general, the research ends advertised.

Global LCD TV Panel Market Report 2022 is spread across 117 pages and provides exclusive vital statistics, data, information, trends and competitive landscape details in this niche sector.

The information for each competitor includes – Company Profile, Main Business Information, SWOT Analysis, Sales, Revenue, Price and Gross Margin, Market Share.

LCD displays utilize two sheets of polarizing material with a liquid crystal solution between them. An electric current passed through the liquid causes the crystals to align so that light cannot pass through them. Each crystal, therefore, is like a shutter, either allowing light to pass through or blocking the light. LCD panel is the key components of LCD display. And the price trends of LCD panel directly affect the price of liquid crystal displays. LCD panel consists of several components: Glass substrate, drive electronics, polarizers, color filters etc. Only LCD panel applied for TV will be counted in this report.

Due to the COVID-19 pandemic, the global LCD TV Panel market size is estimated to be worth USD 53490 million in 2021 and is forecast to a readjusted size of USD 53490 million by 2028 with a CAGR of 2.2% during the review period. Fully considering the economic change by this health crisis, by Size accounting for (%) of the LCD TV Panel global market in 2021, is projected to value USD million by 2028, growing at a revised (%) CAGR in the post-COVID-19 period. While by Size segment is altered to an (%) CAGR throughout this forecast period.

Global LCD TV Panel key players include Samsung Display, LG Display, Innolux Crop, AUO, CSOT, etc. Global top five manufacturers hold a share over 80%.

The global LCD TV Panel market is segmented by company, region (country), by Size and by Application. Players, stakeholders, and other participants in the global LCD TV Panel market will be able to gain the upper hand as they use the report as a powerful resource. The segmental analysis focuses on sales, revenue and forecast by region (country), by Size and by Application for the period 2017-2028.

Global LCD TV Panel market analysis and market size information is provided by regions (countries). Segment by Application, the LCD TV Panel market is segmented into United States, Europe, China, Japan, Southeast Asia, India and Rest of World. The report includes region-wise LCD TV Panel market forecast period from history 2017-2028. It also includes market size and forecast by players, by Type, and by Application segment in terms of sales and revenue for the period 2017-2028.

The report introduced the LCD TV Panel basics: definitions, classifications, applications and market overview; product specifications; manufacturing processes; cost structures, raw materials and so on. Then it analyzed the world’s main region market conditions, including the product price, profit, capacity, production, supply, demand and market growth rate and forecast etc. In the end, the report introduced new project SWOT analysis, investment feasibility analysis, and investment return analysis.

LCD TV Panel market size competitive landscape provides details and data information by players. The report offers comprehensive analysis and accurate statistics on revenue by the player for the period 2017-2021. It also offers detailed analysis supported by reliable statistics on revenue (global and regional level) by players for the period 2017-2021. Details included are company description, major business, company total revenue and the sales, revenue generated in LCD TV Panel business, the date to enter into the LCD TV Panel market, LCD TV Panel product introduction, recent developments, etc.

The report offers detailed coverage of LCD TV Panel industry and main market trends with impact of coronavirus. The market research includes historical and forecast market data, demand, application details, price trends, and company shares of the leading LCD TV Panel by geography. The report splits the market size, by volume and value, on the basis of application type and geography. Report covers the present status and the future prospects of the global LCD TV Panel market for 2017-2028.

Global LCD TV Panel Market report forecast to 2028 is a professional and comprehensive research report on the world’s major regional market conditions, focusing on the main regions (North America, Europe and Asia-Pacific) and the main countries (United States, Germany, United Kingdom, Japan, South Korea and China).

The recent COVID-19 outbreak first began in Wuhan (China) in December 2019, and since then, it has spread around the globe at a fast pace. China, Italy, Iran, Spain, the Republic of Korea, France, Germany, and the US are among the worst-affected countries in terms of positive cases and reported deaths, as of March 2020. The COVID-19 outbreak has affected economies and industries in various countries due to lockdowns, travel bans, and business shutdowns. The global food and beverage industry is one of the major industries facing serious disruptions such as supply chain breaks, technology events cancellations, and office shutdowns as a result of this outbreak. China is the global manufacturing hub, with the presence of and the largest raw material suppliers. The overall market breaks down due to COVID-19 is also affecting the growth of thebaconmarket due to shutting down of factories, obstacle in supply chain, and downturn in world economy.

To Know How COVID-19 Pandemic Will Impact LCD TV Panel Market/Industry- Request a sample copy of the report-https://www.researchreportsworld.com/enquiry/request-covid19/21019731

The report offers exhaustive assessment of different region-wise and country-wise LCD TV Panel market such as U.S., Canada, Germany, France, U.K., Italy, Russia, China, Japan, South Korea, India, Australia, Taiwan, Indonesia, Thailand, Malaysia, Philippines, Vietnam, Mexico, Brazil, Turkey, Saudi Arabia, U.A.E, etc. Key regions covered in the report are North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

For the period 2017-2028, the report provides country-wise revenue and volume sales analysis and region-wise revenue and volume analysis of the global LCD TV Panel market. For the period 2017-2021, it provides sales (consumption) analysis and forecast of different regional markets by Application as well as by Type in terms of volume.

What are the market opportunities and threats faced by the vendors in the global LCD TV Panel market? What industrial trends, drivers, and challenges are manipulating its growth?

Comprehensive company profiles covering the product offerings, key financial information, recent developments, SWOT analysis, and strategies employed by the major market players.

With tables and figures helping analyze worldwide Global LCD TV Panel market trends, this research provides key statistics on the state of the industry and is a valuable source of guidance and direction for companies and individuals interested i

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey